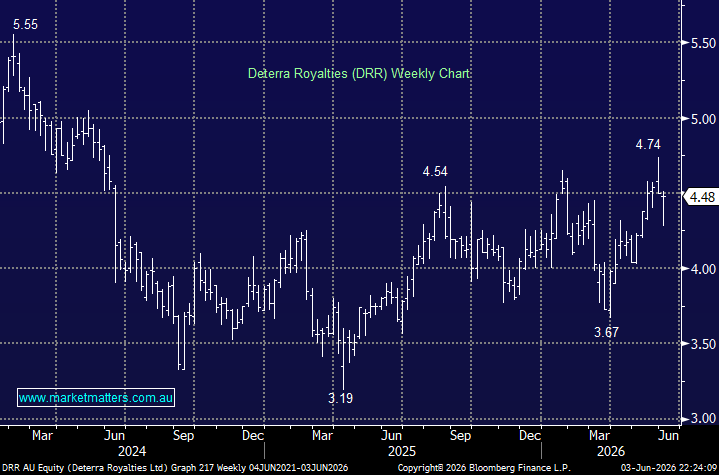

Deterra is another resource business, but it comes with a James Bond-style twist. Deterra is a royalty company that generates revenue primarily from a royalty over BHP’s Mining Area C iron ore operations in the Pilbara, giving investors exposure to iron ore production without the operating risks of mining. The company has expanded beyond iron ore through investments in battery metals, mining royalties and infrastructure-linked assets, creating a more diversified royalty portfolio, but at this stage, ~95% of revenue still comes from iron ore.

Deterra is known for its strong cash generation, capital-light business model and attractive dividend yield, making it a popular income-focused resource investment on the ASX. Last year, DRR yielded 5.7% fully franked, but this yield will fluctuate with the iron ore price; if iron ore enters a prolonged downturn, DRR’s yield will come down with it.

- The key difference versus owning BHP, Rio or FMG is that Deterra gets paid “off the top” of revenue. If iron ore falls from US$120/t to US$80/t, Deterra’s revenue and dividends will decline, but it doesn’t have to absorb rising mining costs or spend billions to sustain operations.

Investors effectively get exposure to the iron ore sector with a cleaner business model, but you shouldn’t expect the dividend to be as stable as a bank or infrastructure stock. However, we continue to adopt a contrarian outlook on the bulk commodity, expecting it to average well above $US100/MT through 2026, as it has done so far.

- We can see iron ore surprising on the upside through 2026, as it already is, suggesting DRR should perform strongly through 2H 2026.

MM is bullish towards DRR around $4.50

Add To Hit List