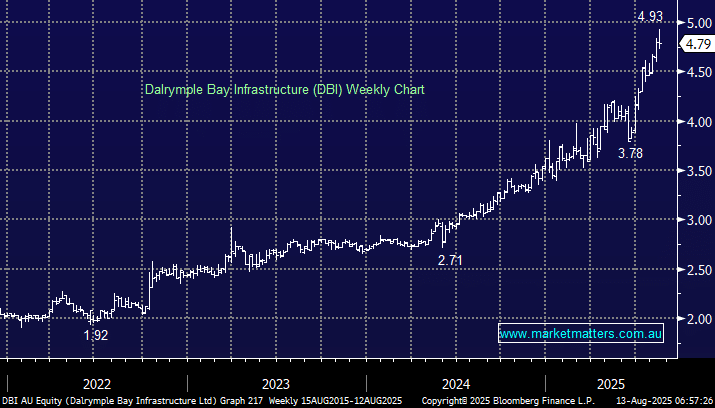

The owner of a large coal export terminal in QLD of the same name, has had a great run in terms of share price, reducing its yield – now at 5% (mostly franked) at current levels. We’ve recently seen a couple of broker downgrades flow through for this reason, with Morgans pulling back their rating to a hold and $4.70 PT yesterday, though that still makes them the most optimistic on the street. Citi and Evans & Partners both retain buys, but with price targets below the current share price, no doubt awaiting results due on the 25th of this month before tweaking their respective calls.

- We were drawn to DBI’s take-or-pay contracts, meaning their contracted coal volumes are paid for irrespective of whether they move coal through the terminal or not, making DBI a stable infrastructure asset, generating consistent earnings that will grow over time.

Having bought shares at $3.37 and accrued nice quarterly dividends along the way, we now pull back our bullish call on the stock, moving to a more neutral position ahead of results. The obvious tailwind now comes from a reduction in the cash rate, expanding the spread that DBI offers relative to cash, and we believe this will keep DBI well supported, though we doubt it will be enough to keep the shares on such a strong upward trajectory.

On a 5% yield, the expected returns are now lower, although they are aiming for annual distribution growth of 3% to 7%. This is a steady infrastructure stock that is delivering, with long-term contracted earnings. While we doubt that DBI will re-produce it’s stellar FY25 returns in FY26, we still think it’s a position worth holding.

MM has turned more neutral on DBI ~$4.75

Add To Hit List