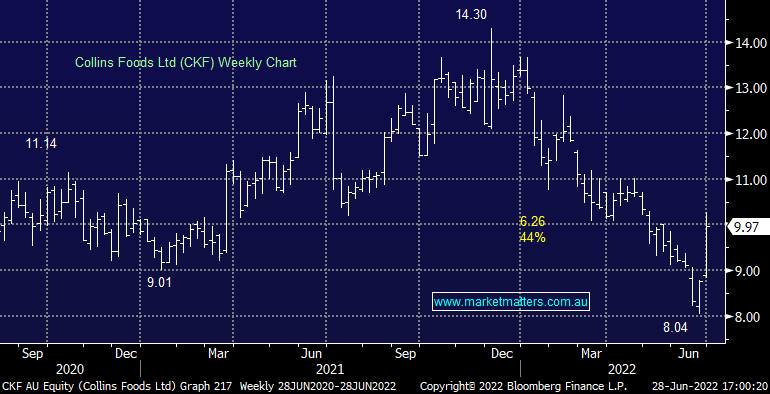

CKF +11.52%: Full-year results out for the KFC franchise owner today were impressive despite what was largely expected to be a soft period. Revenue was a slight beat at $1.18b, but NPAT was around 5% ahead of expectations and up 68% in the year. Same-store sales growth was strong across the board for KFC Australia (+1.4%) and Europe (~17%), though the junior Taco Bell segment saw negative comps. Margins were solid despite cost pressures as they put through price hikes to offset food and wage cost increases. FY23 has also started well with same-store sales growth continuing to impress, up 4% in Australia and 15% in Europe. They expect to open over 20 stores across their brands in FY23 to further drive growth.

MM is neutral CKF

Add To Hit List