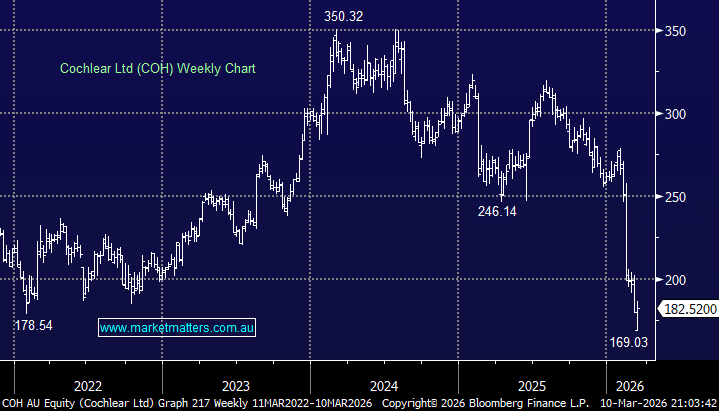

COH has more than halved from its 2024 high, and it now trades on its lowest valuation of the decade, despite revenue continuing to climb from $1.6bn in 2022 to a forecast $2.7bn by 2027. However, the market showed little patience during the recent reporting season, with the hearing device maker falling ~25% in February after a comparatively modest ~5% 1H profit miss. The miss was driven by weaker revenue, which came in ~4% below consensus, alongside margin pressure from a higher mix of lower-priced China VBP sales and the manufacturing transition to the Nexa platform. The recent news has been poor from COH, but it’s now priced for ongoing disappointment. The rhetoric from the company was, as would be expected, more positive moving forward.

COH flagged the strong Australian dollar ($A) as a key headwind, estimating it could reduce FY26 profits by around $30m if current exchange rates persist, despite existing hedging. Management reiterated its long-term guidance of ~10% sales growth and an 18% profit margin, though margins are expected to sit slightly below this level in FY26 due to FX pressures and the rebuilding of short-term incentive provisions. The company plans to manage costs more tightly in FY27 to move back toward the 18% margin target.

Operationally, market share declined in the first half as competitors responded to COH’s efforts to increase pricing for its new Nexa implant, although the company said the outcome was largely expected given discounted pricing offered to some hospitals to support volume. Management remains confident its share will recover through 2026, supported by modest price increases for Nexa and stronger second-half sales. While Asia-Pac revenue fell due to sharply lower pricing in China, volumes remained strong under China’s volume-based procurement program, and the company believes it has maintained solid market share in the region.

Elsewhere, first-half service revenue was softer but expected to rebound in the second half, supported by product upgrades and new device availability. Gross margins were temporarily pressured by Nexa manufacturing ramp-up and lower-priced Chinese sales, while the acoustics segment lost share in the US and UK following a rival product launch, but is expected to recover later in the year. Cash flow was also impacted by higher inventories ahead of the Nexa rollout, which should normalise in the June half and allow the company to restart its share buyback program.

NB Nexa is COH’s latest cochlear implant platform, designed to improve hearing performance and connectivity while supporting the company’s next generation of sound processors.

chart

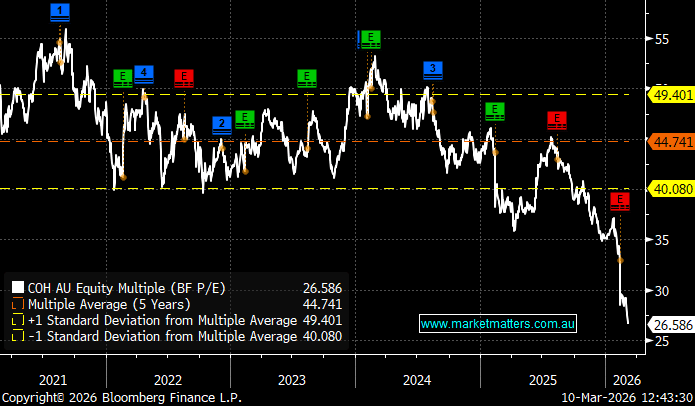

Cochlear Ltd (COH) Valuation over the last 5-Years- Source Bloomberg

chart

Cochlear Ltd (COH) Valuation over the last 5-Years- Source Bloomberg

Despite the slower rollout, Nexa should drive market share gains and support a return to stronger earnings growth. This should be helped by improving momentum in the Services and Acoustics segments. While the stronger $A remains a headwind, we think the outlook for renewed growth supports a higher valuation, particularly with the stock trading significantly below its recent average multiple. However, with Service revenues disappointing for the fourth consecutive reporting period its not surprising investors are cautious toward COH, not helped by the updated guidance, which indicates each 1% move in the $A against key currencies now reduces group profit by a similar magnitude, highlighting increased sensitivity to FX, and MM is bullish towards the $A.

COH has been a market favourite over recent years, akin to CSL, but neither can make it into our hitlist at this stage.

- We can see COH trading between $160 and $200 until we see more evidence that key financial metrics have picked up in the 2H, something the company has strongly alluded to, but the proof will be in the pudding.

MM is mildly bullish towards COH ~$180

Add To Hit List