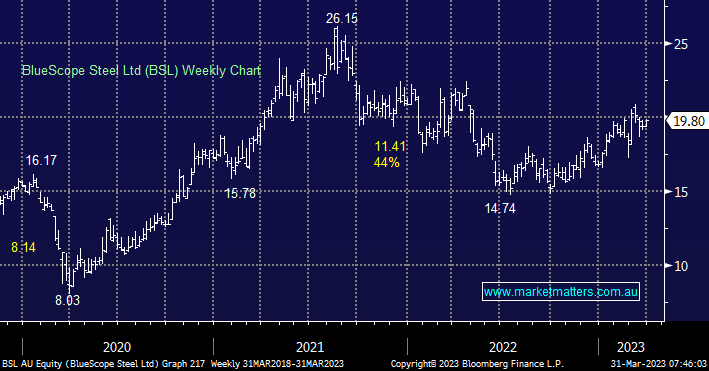

BSL is Australia’s largest steel company which focuses on flat steel products including slab, hot rolled coil, and plate. The company’s main facilities include the North Star steel plant in Ohio, USA, and the Port Kembla Steelworks, the largest steel production facility in Australia plus it operates a US$1.36bn JV with Nippon Steel. Profitability has recovered in recent years as rising steel margins and strong residential construction improved end demand but the latter is in question in the short term as high-interest rates weigh on building activity.

BSL’s 1HFY23 result delivered in February was broadly in-line but was overshadowed by weaker-than-expected 2HFY23 EBIT guidance of A$480-550m however the market shrugged this off within a fortnight. We cannot discount the risks around a recession through 2023/4 but over recent months BSL has already experienced significant underperformance when compared to its key peers Nucor (NUE US) and Steel Dynamics (STLD US) leaving plenty of room for pickup by the local company.

- We believe Australia will commence a fresh bout of building ASAP as the rental crisis deepens and migration recommences in earnest, a great local backdrop for BSL.

- We like the company’s prospects medium term and believe the next 10% for BSL is on the upside but decent dips on economical fears cannot be discounted.

MM is bullish towards BSL medium term

Add To Hit List