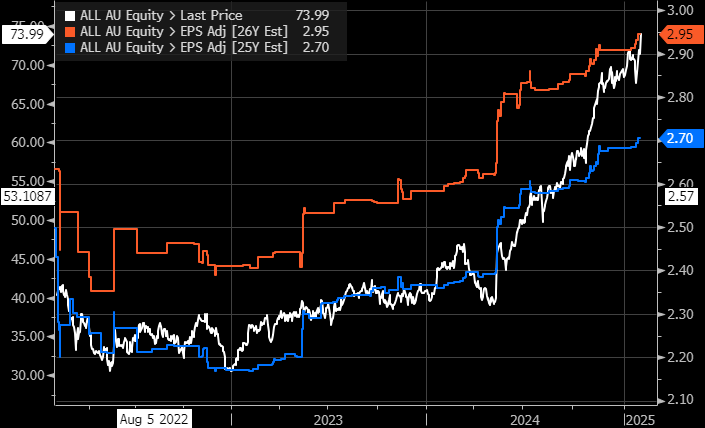

Gaming company ALL rallied +3.7% on Thursday, making new all-time highs, aided by Goldman’s upgrade earlier in the week from Neutral to Buy. The stock may feel rich/extended at first glance, but it’s simply tracked higher inline with earnings expectations, although it is now trading at the top end of its post-GFC valuation, leaving little room for disappointment. ALL delivered a solid FY24 result late last year, and we liked how they have decided to go back to what they know best: concentrating on finding opportunities in regulated gaming, i.e. poker machines and casino-style online games. It is a great company but not one we want to chase at current levels, and going out on a limb, another $8-10 pullback wouldn’t surprise us in 2025.

- We underestimated how far ALL would rise in 2024/5, but we don’t like the risk/reward above $70.

NB: The blue line shows consensus EPS forecasts for FY25, and the orange line plots the same for FY26. These are forward looking assumptions, based on an aggregation of analysts’ forecasts.

MM is neutral ALL around $74

Add To Hit List