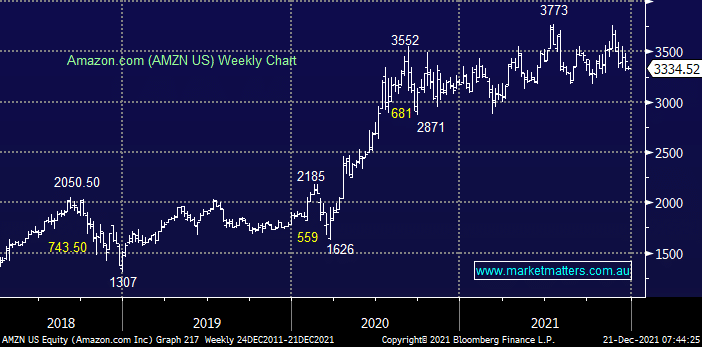

Amazon is the undoubted underperformer of the 3 having struggled to make significant gains over the last year. Amazon had a relatively tough last quarter due to supply chain issues, rising wage costs / labour shortages and the elevated costs of goods the e-retailer sells but via its Amazon Web Services (AWS) and Amazon Marketplace it should be well positioned into 2022. That said, we do remain conscious that like much of the sector it’s not cheap and definitely vulnerable to a “bond tantrum”.

Similar to Apple and Microsoft, given valuation we might trim our position into new highs but similarly 10% lower we would consider increasing once again.

MM remains long and bullish AMZN

Add To Hit List