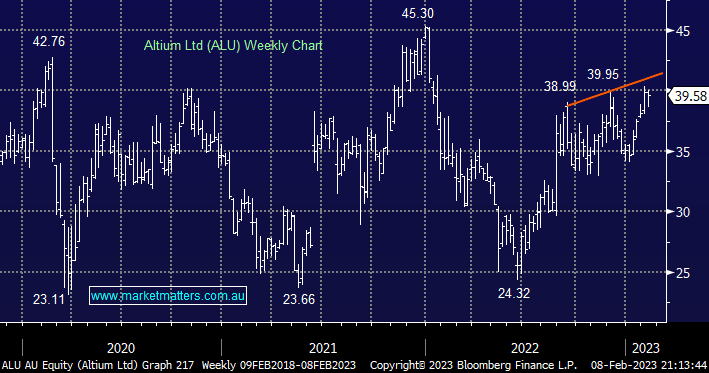

The MM Flagship Growth Portfolio has been overweight the Australian Tech Sector since Q4 of 2022, this $5.2bn company is starting to feel expensive trading on an Est valuation of 55.6x for 2023 – a very crude measure to use for growth companies but it serves our point in this instance. It is a company that has delivered, where many haven’t, and the growth from here remains attractive i.e. this is a company we like a lot, with a great product, that is making money and growing, but we think this is largely captured in the price.

- We like ALU but it’s starting to feel rich as it approaches $40 just when MM is looking to pare back our tech exposure i.e. we may trim our 5% position or simply take profit depending on alternatives at the time.

MM is considering taking profit on ALU around $41

Add To Hit List