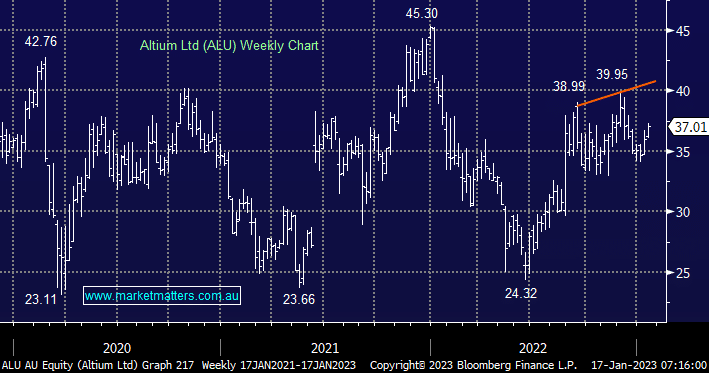

ALU has struggled compared to its peers over recent weeks as buyers appear to have gone in search of bargains as opposed to chasing the top performers. This Printed Circuit Board (PCB) design platform reported excellent FY22 results last August, revenue was $221m and EBITDA $81.1m while their FY23 guidance was also significantly better than consensus hence it’s unlikely we will be selling this particular holding into weakness.

- We are now considering reducing/selling our 5% holding in ALU ideally above $38.

MM is mildly bullish ALU around $37

Add To Hit List