The printed circuit board design software provider was out with 1H23 results at 5 pm last night which is their usual time of release, and the result was broadly in line from both a revenue and profit perspective while they maintained their FY23 guidance which is for revenue of $255-265m – a growth rate of 15-20% on FY22. The 1H was a solid one given the challenging operating conditions, but the stock has run up into the result which makes us more cautious.

Revenue of $119.5m (v $121m consensus), although the currency was a headwind with revenue of $124.8m in constant currency terms, EBITDA margins expanded from 34.1% to 36.2% and that drove post-tax profit of $29.6m (v ~$30.6m consensus). An increase in the dividend to 25cps (up 19%) was a nice sweetener but not why we own the stock. They also said they remain on track towards their aspirational FY26 revenue target of $500m. All in all, a good result, a smidgen light on, and given the way the share price has moved into the result, we may see some profit taking.

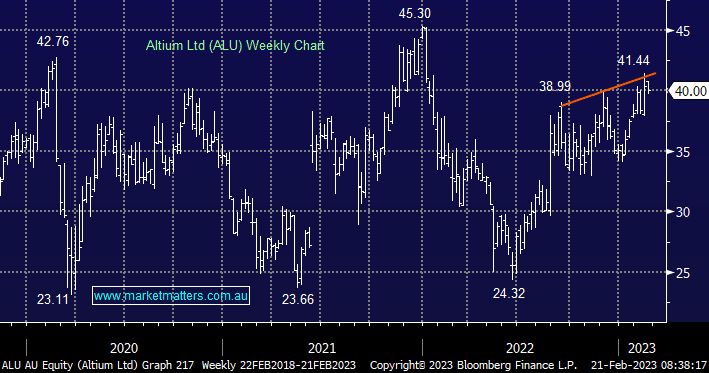

MM is bullish ALU, however, may trim our position if it trades up around ~$41

Add To Hit List