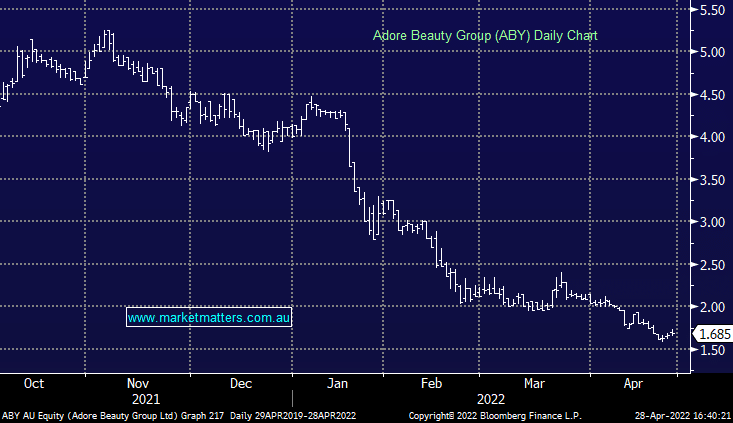

ABY +1.51%: the beauty and personal care retailer’s 3rd quarter numbers showed solid growth coming through the business, despite comping elevated COVID sales in the prior period. Revenue was up 9% and active customers up 7% in the period. Investment in mobile and loyalty programs appear to have been fruitful and supports near term growth. Managing the supply chain remains a key risk. However, they are well funded and have no debt on the balance sheet. The numbers place the business well to hit consensus revenue expectations of $208.4m vs $155.8m in the first 9 months – the shares just remain completely unloved!

MM remains patiently long ABY in our Emerging Companies Portfolio

Add To Hit List