Previous investor favourite A2 Milk (A2M) has rallied toward five-year highs this week following a well-received first-half result that defied China’s declining birth rate – its most important market. An expanded product range in China drove revenue well ahead of expectations, prompting the company to upgrade its full-year guidance. While China’s birth rate remains at record lows, a structural headwind for the business, A2M has demonstrated an ability to offset demographic pressure through product innovation and brand strength.

- A2M still receives ~60% of its revenue from infant milk formula sales in China, illustrating the importance of the country.

a2 Milk reported net income for the first half-year that was a clear beat, leaving analysts pondering whether they’ve misread the China story, with upgrades having poured through over the last 48 hours.

- Net income NZ$112.1 million, +9.4% YoY, a +8.3% vs estimates.

- Ebitda margin 15.6% vs. 15.6% YoY.

- Revenue NZ$993.5 million, +19% YoY.

On the earnings call, management addressed concerns around China’s 2025 birth rate, highlighting multiple offsetting growth drivers. These include continued market share gains supported by strong execution and new product development, notably Genesis, two new China-label launches and the first upgrade to the a2 Platinum formulation since 2022. The English-label segment continues to outpace the China-label market, benefiting A2M given its stronger share in the former (19.1% vs 5.6%). Geographic expansion remains robust, with Vietnam sales up 128% on the prior corresponding period and additional markets in the pipeline, alongside category expansion into seniors, kids and paediatric supplements. Management also pointed to lower breastfeeding rates supporting formula penetration, while noting that Stage 1 sales in 1H26 were likely constrained by supply issues that have since been resolved.

- At MM, we always find it encouraging to see a business performing stoically through macro headwinds – it often bodes well for the future.

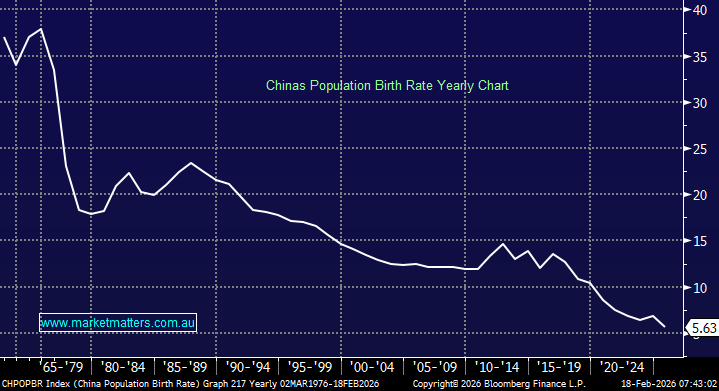

China’s record-low birth rate reflects five key factors: high living and education costs that deter larger families; weak economic confidence and youth unemployment; shifting social norms, including later marriage and career prioritisation; the long-term legacy of the one-child policy reducing the cohort of women of childbearing age; and rapid urbanisation, which typically correlates with smaller family sizes. Collectively, these structural forces make a near-term demographic rebound unlikely despite policy support measures (government incentives). Hence, when we evaluate A2M, we believe a recovery in this birth rate shouldn’t be factored into any assumptions.

chart

Chinas Population Birth Rate – annual per 1000 people in the population

chart

Chinas Population Birth Rate – annual per 1000 people in the population

CEO David Bortolussi summed up this week’s result well, saying the market has underestimated the resilience of the industry after strengthening sales in China boosted earnings, with their upgraded outlook meaning they are now on track to achieve their NZ$2 billion medium-term sales ambition in FY26, a full year ahead of plan. The rally in the stock comes after the firm’s shares plunged in January on news that China’s birth rate had fallen to its lowest since the formation of the People’s Republic in 1949.

The China-label segment accounts for roughly 80% of the total Chinese infant formula market, yet A2M holds just over 5% share, highlighting significant room for expansion. Management indicated it plans to broaden its offering to as many as four products, supported by the recent acquisition of the a2 Pōkeno facility, to better penetrate this dominant segment. Another potential tailwind for the NZ-based business in the years ahead.

- We are optimistic towards A2M as its strong execution looks likely to continue.

MM is bullish on A2M around $9.60

Add To Hit List