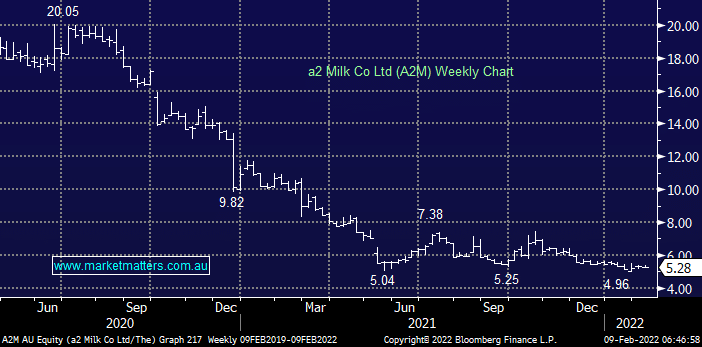

A2M has gone from hero to villain in just 18-months after a number of issues conspired to see the stock plunge by around 75%, fortunately we tried to pick a bottom after the stock had already endured 80% of its losses but the trend would have been our friend here if we had simply stayed away. We’ve actually held A2 on multiple occasions over the past ~5 years and we’re down -10.61% in aggregate, not too bad however our current holding down ~35% is causing us some pain.

Moves in China has seen the daigou resell channels dry up plus COVID has caused significant disruptions between Australia & China, although the later should start to improve through 2022. The company was caught holding excessive inventory levels it couldn’t sell and we’ve seen the stock rerated in a major way. While we believe the worst is behind A2M and new management have reset market expectations – cleared the decks as they say – our lingering concern is around lower birth rates in China negatively impacting the size of the overall opportunity.

Having said that, and with take-over rumours surfacing on an almost monthly basis another test of thee $7-8 feels a strong possibility i.e. we are resigned to losing with A2M but our feeling is things will improve into 2022. They report results on 21st February.

MM is mildly bullish A2M from under $5.50

Add To Hit List