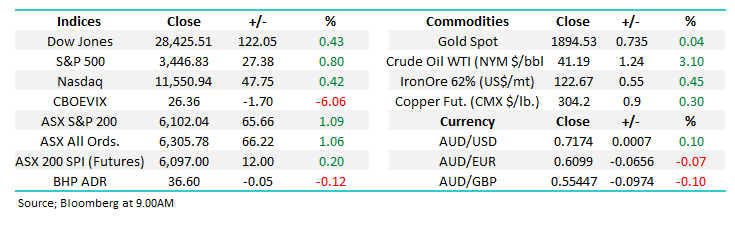

Is the Healthcare Sector poised for some catch up? (CWN, SGR, RHC, CSL, COH, RMD, ANN)

Another strong session for Australian stocks on Thursday taking the weekly gains into today above 320-points / 5.6%, we had a helping hand this time from overseas markets but the budget appears to have laid the foundations for the ASX200 to finally break above the psychological 6200 area. The rally wasn’t as broad based yesterday with over 30% of the index closing lower but the heavyweights rallied and those stocks which did advance noticeably did so by far more than the losers, hence the index again rallied more than 1% closing above 6100 for the first time in a month.

The theme for the week has remained pretty consistent into Friday, the banks and IT stocks have been strong while the defensive Real Estate and Utilities struggled. If we continue along this path and the index can hold above 6100 today it will be an extremely encouraging sign that the markets poised to break out to the upside. However, I would caution we have previously felt this was likely over recent months, hence we must remain respectful of the major resistance lurking only 1.6% higher.

I’m really sorry to bring it up again but NSW registering 12 fresh cases of COVID yesterday is clearly a step in the wrong direction, suddenly all those long weekend trips interstate and to the beach are being called into question. This is the first time that an open NSW has registered more cases than the closed down Victoria in many months. The Australian economy needs a healthy NSW to shoulder the burden until Victoria reopens, I hope we’ve just seen a numerical aberration. I was meant to be in QLD as I type this, sailing in the Whitsundays, something we’ve put off for another year – lets hope that timeframe doesn’t turn out to be an optimistic one.

MM remains bullish stocks into 2021.

ASX200 Index Chart

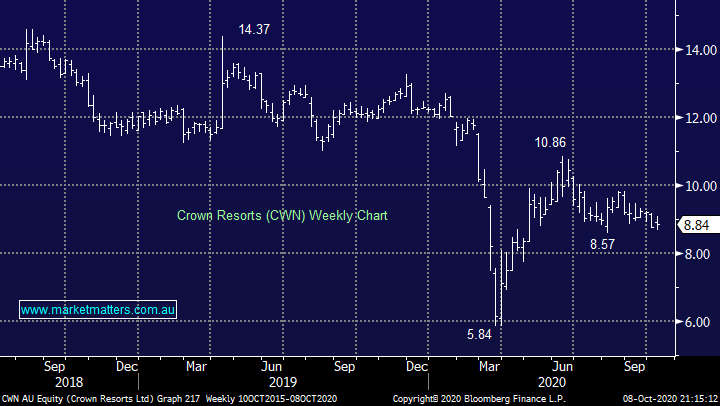

Crown and Jamie Packer have endured a very public tough few days amid concern that they may be stripped of their casino licence in Sydney, but the share price remains fairly resilient implying that the market does not believe that will be the case. I tend to agree given the $$ this will bring in for depleted Govt coffers. I was chatting last night over dinner to my Father in Law about this and I’ve given it more thought on the ride in this morning.

There are number of different ways this can play out from a stock perspective, but our opinion is pretty simple:

1 – The position in CWN held by Consolidated Press (Packer) is now on the market which raises an initial obvious question : which entity that the regulatory authorities will approve has at least $1.5bn to take his holding below 10%, or indeed $2.2bn the buy the lot – that’s assuming that the transaction takes place at yesterday’s closing price which is an optimistic view.

2 – Over recent years several buyers have circled the company, including Wynn Resorts and Lawrence Ho’s Melco, as Packers interest in the business appears to diminish, but nothing’s been crystallised. Alternatively his stake could be sold to existing shareholders / institutions via a placement and although that’s likely to be easier / quicker the exit price would probably be lower, especially as the migration to ethical investing has seen the pool of buyers steadily diminish over recent years.

There’s obviously plenty of water still to flow under the bridge but we believe Packers hands are up as a seller, I wonder who UBS, Goldman Sachs et al are talking to with regard to making an offer. In our opinion the stocks worth more with Packer reduced to sub 10%, or indeed out altogether. If we get a quality international operator come on board the stock could pop higher overnight. Also, CWN is leveraged to an eventual Victoria recovery, it feels to us like the stocks very close to some “good news”. I feel accumulation into weakness will look good at some stage in the next 6-months, ideally lower but in situation plays it gets tricky to pinpoint exact ideal entry levels.

MM likes CWN on the backfoot towards $8.

Crown (CWN) Chart

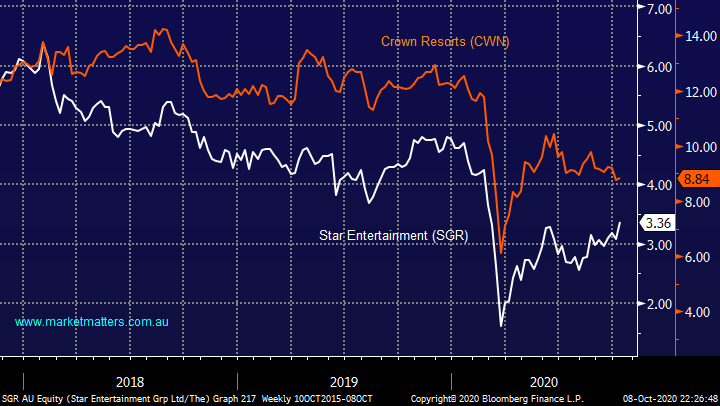

MM owns competitor Star Entertainment (SGR) in its Growth Portfolio as a proxy for an economic turnaround, so far so good but it begs the question is there an opportune time to switch from SGR to CWN?

MM is bullish SGR initially targeting $4.

Star Entertainment (SGR) Chart

The comparative chart of the 2 stock prices shown below illustrates that from a historical perspective CWN is slowly becoming more attractive but switching is not an obvious consideration today, especially considering the risks at CWN e.g. a large discounted placement to existing shareholders.

At today’s prices MM still prefers SGR over CWN.

Star Entertainment (SGR) v Crown Resorts (CWN) Chart

Overseas Indices & markets

Overnight US stocks continued their recovery led by the Energy Sector which rallied by almost 4%, encouragingly all 11 sectors of the S&P500 closed positive even while the index only rallied +0.7%. The Dows now only ~4% below its pre-COVID all time high and we believe it will follow the broad-based S&P500 & tech NASDAQ by breaching this milestone into Christmas.

MM continues to believe US stocks have found a significant short-term low.

US Dow Jones Index Chart

Overnight crude oil rallied over 3% taking the Energy Sector along for the ride, MM is still bullish in the short-term and were targeting an initial ~10% rally to fresh post March highs – Beach Petroleum (BPT) remains our preferred exposure to the sector.

MM remains the Energy Sector.

Crude Oil December 2021 Chart

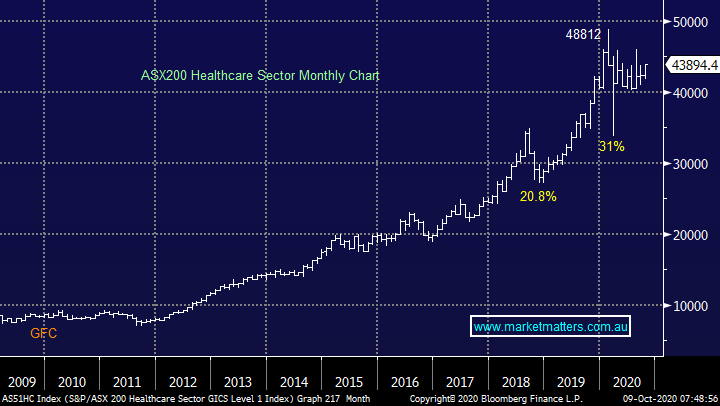

Is it time to buy the Healthcare Sector?

Yesterday the Healthcare Sector rallied +2.6%, only beaten on the day by the IT stocks, its been a while since this previously loved group has caught my eye in the outperformance enclosure. In our opinion there are 3 standout reasons that the likes of CSL Ltd (CSL) have struggled over the last 6-months e.g. over this period CSL has fallen -9% while even the embattled CBA has rallied over +10%.

1 – After being a huge outperformer post the GFC investors and momentum traders were complacently long the likes of CSL Ltd (CSL), ResMed (RMD) and Cochlear (COH), history tells us this was an accident waiting to happen.

2 – As COVID hit the world the sector significantly outperformed the market for obvious reasons, it had all the characteristics of a blow-off top.

3 – Most of the Healthcare Sector have significant offshore earnings which has been a massive tailwind over the last decade but since March this has reversed and again we believe investors were significantly overweight “$US earners” which in our opinion both is & was wrong, MM has been bullish the $A all year.

MM feels the Healthcare Sector is now due for a period of market performance after struggling over the last 6-months.

Australian Dollar ($A) Chart

Hence if we assume that the sector will basically perform in-line with the ASX moving forward and MM is bullish equities then the subsequent read through is there will be some opportunities within the sector into 2021.

MM is bullish the ASX and Healthcare Sector into 2021.

ASX200 Healthcare Sector Chart

Today I have briefly looked at 5 major members of the sector to evaluate if / when we may consider increasing our exposure to Healthcare.

1 Ramsay Healthcare (RHC) $69.49

Private hospital operator RHC like many companies has experienced a tough 2020 due to COVID and the subsequent decrease in elective surgeries while costs went up. However, as the world looks forward to a vaccine in 2021 we believe the stocks perfectly positioned to test its all-time high ~$80.

MM remains bullish and long RHC in our Growth Portfolio.

Ramsay Healthcare (RHC) Chart

2 CSL Ltd (CSL) $298.94

Heavyweight CSL is undoubtedly a great company but it was suffering from all 3 of the points raised earlier plus its valuation simply became way too stretched. However, we do believe the stocks now bracing for a 10-15% rally, this is arguably the conservative play in the sector but we would be more comfortable leaving some room to average into another dip lower towards $250.

MM likes CSL but would leave room to average under $260.

CSL Ltd (CSL) Chart

3 Cochlear (COH) $208.85

Hearing implant business COH reported a 6% drop in sales over the last financial year which included the savage COVID quarter, not too bad in our opinion. With a kick up in elective surgeries the stock should be able to rally 10-15% in a firm market but its vulnerable if a vaccine is not forthcoming.

MM is neutral to bullish COH.

Cochlear (COH) Chart

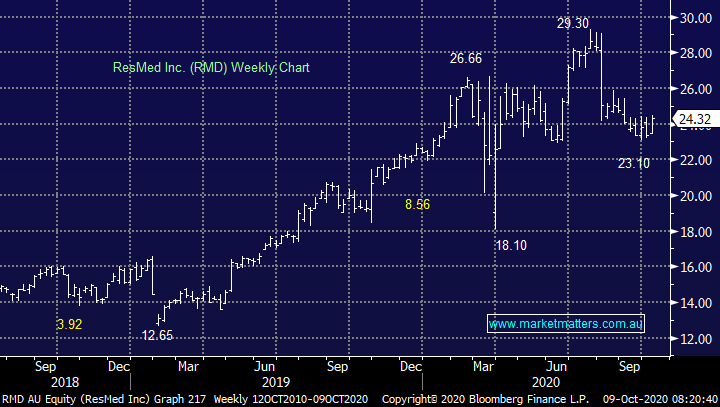

4 ResMed (RMD) $24.32

Sleep disorder business RMD delivered solid 4th quarter and full year results in August but cautious comments from the company didn’t excite investors who had the business priced for ongoing strong growth. Short-term the stock looks set to test $26 but it’s definitely not on our shopping list.

MM is mildly bullish RMD short-term.

ResMed (RMD) Chart

5 Ansell (ANN) $38.81

We hopefully are approaching a post COVID world but 2020 will not be forgotten in a hurry and we believe health and safety business ANN is well positioned for this new look future – ANN looks set to rally a minimum of 10% short-term.

MM is bullish ANN targeting fresh all-time highs.

Ansell (ANN) Chart

Conclusion

MM likes the Healthcare Sector into 2021 with our order of preference of stocks looked at today : RHC, ANN, CSL, COH and RMD, at this stage only the first 3 are on our watch list and we already own RHC.

Have a great day!

James & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. All prices stated are based on the last close price at the time of writing unless otherwise noted. Market Matters does not make any representation of warranty as to the accuracy of the figures or prices and disclaims any liability resulting from any inaccuracy.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The Market Matters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.