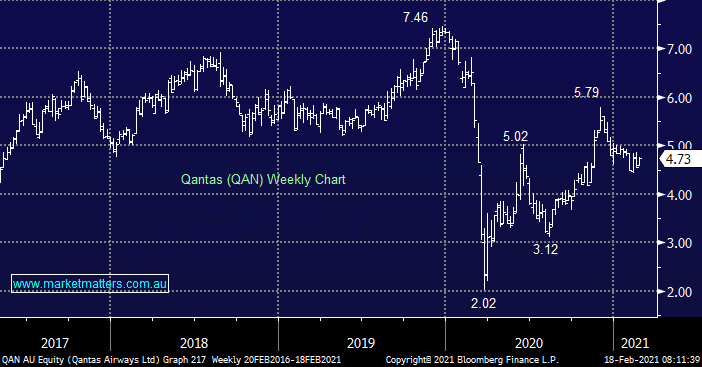

It’s easy to comprehend the struggles QAN has endured over the last 12-months but under $5 we must question if too much bad news is priced into the iconic airline. The exciting factor for QAN is the pandemic allowing the company to totally rebase their costs putting them in a position to emerge strongly from COVID. The other positive aspect is around competition. Virgin is now in the hands of private equity who are very much aligned with the QAN way of thinking i.e. all about profits making them a very rationale competitor whereas the virgin of old was not, and we know where that got them!

Domestic travel is already forecast to increase to almost 70% by Christmas with leisure demand leading the way – many people I know are itching for a holiday! Domestic is the main driver of QAN earnings, international is nice to have but nowhere near as important.

The risk / reward into current weakness is attractive, we can see $6 being tested this year as the trading backdrop improves as the vaccine is rolled out both at home and overseas.

MM likes QAN around current levels

Add To Hit List