Equities panic on cue, time for opportunities (EVN, GDX US, SIQ, TBF US)

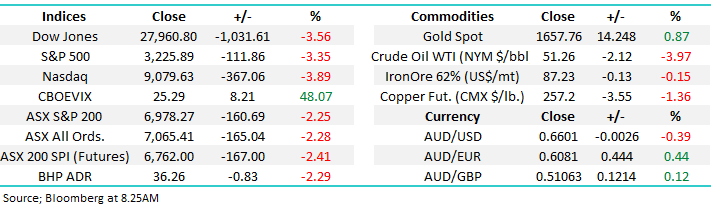

Yesterday the ASX200 was positively hammered enduring its largest decline in 6-months, stocks gapped lower in the morning and basically retreated all day finally closing down a painful 160-points / -2.25% we witnessed volume selling across the board, with only 7% of the index closing positive & over half of these winners resided in the safety of the gold sector. I’m sure all subscribers know by now that the weakness was attributed to fears that the coronavirus was spreading outside of China, no real surprise to MM we wrote the below only last Friday morning:

“Our Gut Feel at MM is we will see another bout of selling on fears around the coronavirus in the coming few weeks, it’s not going away anytime soon.” - MM Friday 21st February.

Stock markets have performed an about face on the pricing of risk, last week the coronavirus was being dismissed as a bad cold, this morning the Dows plunged over 1000-points and I’m watching almost blind panic in many parts of the market – our prediction of a volatile 2020 where investors should follow the uncomfortable path and buy weakness / sell strength feels still on the money – people have stopped talking about a vaccine but doctors will solve this conundrum.

So far so good, equities are following our anticipated path hence we are likely to be very active today / overnight – I have endeavoured to keep things simple stupid (KISS) this morning outlining our plans:

1 – Equities have been enjoying a liquidity driven bull market for over a decade – in the AFR I read on the weekend that property buyers are still sitting on buckets of cash looking for things to buy, sounds like stocks last week. We believe this cash has retreated into its shell but it remains on the sidelines.

2 – Last week MM said that the risk / reward favoured the sellers around 7200 as zero percentage risk of an escalation from the coronavirus was being built into stocks, what an understatement! We increased our cash position from 1% to 12%, we believe todays the time to reverse this more conservative stance.

3 – We’ve been of the opinion that stocks would rally in 2020 in a choppy staircase style manner with our ideal retracement target the 6900 area, just over 1% below yesterdays close – this morning the ASX200 looks set to open below our 6900 buy zone but panic is rarely a pure science.

4 – We believe central banks will step in with some bazooka like stimulus fairly soon to alleviate fears of a virus led plunge in global growth, China’s PBOC have already been rattling their cage.

MM is now in “Buy Mode” looking to increase our exposure to equities.

Overnight US stocks were hammered with the Dow falling over 1000-points, the SPI is calling the ASX200 to open down well over 2% / 170pts today, exciting times ahead.

Today we have written a simple but important report outlining what buttons we anticipate pressing over the next 24-hours, I think it’s going to be very busy and a clear actionable plan is imperative for all investors, ourselves included. Subscribers will notice that while we are looking to be aggressive with our asset allocation overall, we have been relatively conservative with our stock selection.

ASX200 Chart

Global Indices

US equities were hammered last night with the tech-based NASDAQ tumbling almost 4% to test our 9000 buy area in rapid fashion, everything’s happening faster at the moment which ties in with our volatile call for 2020. Assuming our interpretation is correct there is now 1 important point to bear in mind:

1 – The trend is up, and sharp pullbacks are buying opportunities, this is not a time to panic.

MM is now bullish US stocks looking to increase our equities exposure.

US NASDAQ Index Chart

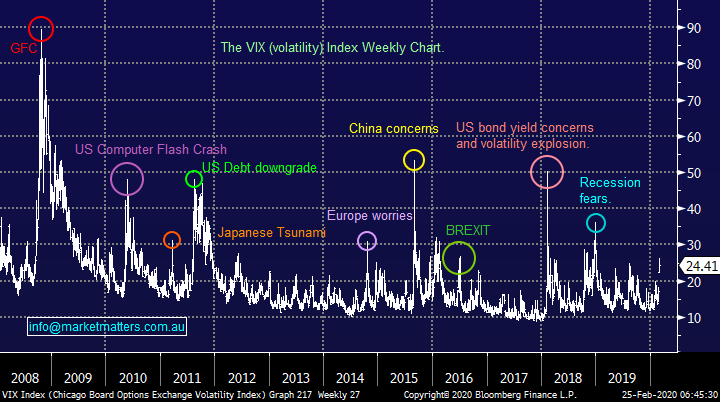

To put things in perspective the chart below of the most closely watched “Fear Gauge” the VIX shows the coronavirus is now worrying investors to the same degree as the Japanese Tsunami in 2011 and BREXIT.

US Fear Gauge (VIX) Index Chart

Market Matters Growth Portfolio

As mentioned earlier MM is sitting on 12% cash in our Growth Portfolio plus a defensive 3% exposure to gold stock Evolution Mining (EVN) : https://www.marketmatters.com.au/new-portfolio-csv/

Firstly, let’s look at the stock we are likely to sell, no surprises there!

Evolution Mining (EVN) $4.56

MM has not enjoyed our gold ride from Australian stocks in 2020, while gold in $A terms hits all-time highs and global gold ETF’s remained firm the likes of Newcrest (NCM) and Evolution (EVN) have significantly underperformed. Aided by the recent virus panic EVN is now sitting 36% above its recent low, a relief to us that it has managed some degree of a recovery.

MM is looking to close out our EVN position into current strength.

This sale will take our cash position up to 15%.

Evolution Mining (EVN) Chart

During this morning’s panic the VanEck gold Miners ETF (GDX US) has hit our medium-term target area and rejected it, closing near the lows of the day.

MM is looking to liquidate our gold exposure across all portfolios today.

VanEck Gold Miners ETF (GDX US) Chart

Banks

MM has made no secret that we like the banks through 2020 / 2021, while the sector has been cheap for some time, we are now seeing more green shoots in terms of earnings, plus of course their fully franked dividends, our plan this morning:

1 – Increase our holdings of Westpac (WBC) and National Australia Bank (NAB).

2 – Buy more internationally focused Macquarie Bank (MQG), ideally around $140.

ASX200 Banking Index Chart

Conclusion (s)

MM is looking to move back to an overweight exposure to equities with the following in our sights:

1 – Sell evolution Mining (EVN).

2 – Adding to NAB & WBC, plus buying MQG.

3 – Average energy exposure through Beach Petroleum (BPT)

*Watch for alerts

Income Portfolio

MM is sitting on 4.5% cash in our Income Portfolio : https://www.marketmatters.com.au/new-income-portfolio-csv/

Overnight we saw US bond yields make all-time lows coinciding with our medium-term forecast hence we believe it’s time to move slightly up the risk curve for our Income Report i.e. take profit on the CBAPF and increase our exposure to BHP and RIO plus also buying Smart Group (SIQ) which is forecast to yield 6.2% fully franked moving forward.

US 30-year Bond yields Chart

Conclusion (s)

MM is looking to move slightly up the risk curve in search of quality sustainable yield into today’s weakness:

1 – Sell: take profit on our CBAPF Notes as previously flagged.

2 – Buy: SmartGroup (SIQ) and increase our holdings in BHP Group (BHP) and RIO Tinto (RIO).

*Watch for alerts

SmartGroup (SIQ) Chart

MM International Portfolio

MM is sitting on 21% cash in our International Portfolio : https://www.marketmatters.com.au/new-international-portfolio/

Todays activity should come as no surprise to subscribers following on largely from recent reports, note we will send out alerts today to give subscribers time to consider.

The chart below illustrates that the major US index the S&P500 has basically hit our 3200-target area hence it’s time to press our buy buttons

US S&P500 Index Chart

Conclusion (s)

MM is looking to increase our equities exposure in the International Portfolio to an overweight stance with the following moves expected:

1 – Take profit on our Barrick Gold (GLD US) and close out our ProShares bearish ETF (SH US) increasing our cash position to 34%.

2 – Buy LVMH Moet Hennessy (MC FP), Microsoft (MSFT US), Salesforce (CRM US) plus UBS Group AG (UBS US) looking for a recovery in the beaten-up European banking sector.

3 – Increase our exposure to Alibaba (BABA US).

*Watch for alerts

MM Global Macro ETF Portfolio

MM is sitting on 41.5% cash in our Global Macro ETF Portfolio : https://www.marketmatters.com.au/new-global-portfolio/

We have been outlining our anticipated points of inflection for a number of different markets throughout our reports in 2020 and the time has arrived, cometh the hour cometh the man…..couldn’t resist throwing that in but will look pretty dumb if things keep unwinding!

ProShares Short 20+ year US Treasury ETF (TBF) Weekly Chart

Conclusion (s)

MM is looking to increase our risk exposure in the Global Macro ETF with the following moves expected:

1 – Take profit on our VanEck Gold Miners ETF (GDX US), close out our iShares Global Silver Miners ETF (SLVP US) & ProShares bearish ETF (SH US) increasing our cash position to 62%.

2 – Buy the ProShares Short 20+ US Treasury ETF (TBF US), NASDAQ Invescco ETF (QQQ US), iShares MSCI Europe Financials ETF (EUFN US), Invesco DB Agricultural ETF (DBA US) and add to our iShares Emerging Markets ETF (IEM US).

Overnight Market Matters Wrap

- The global panic selloff continued overnight as the coronavirus continues to spread widely outside of China, killing 7 in Italy alone.

- All 3 key indices in the US lost over 3%, particularly the tech. heavy Nasdaq 100, meanwhile in the Eurozone, the EuroStoxx, Germany DAX and French CAC all lost ~4% at the end of their trading session.

- Key equity markets are starting to follow and play catchup with the current bond market and their view of a weaker economic growth rate. This can be clearly seen with Italian bonds falling on concerns the virus could lead the country’s economy into recession.

- On the commodities front, crude oil slid into bear market territory, down 3.97% to US$51.26/bbl. while the ‘safe haven’ gold gained towards US$1657.76/oz. and Dr. Copper – a measure of global growth economy is off 1.36%

- BHP is expected to underperform the broader market after ending its session off an equivalent of -2.29% from Australia’s previous close.

- The March SPI Futures is indicating the ASX 200 continue its adventure down the red sea, and open 170 points lower, towards the 6800 level this morning.

Have a great day!

James & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Disclaimer

All figures contained from sources believed to be accurate. All prices stated are based on the last close price at the time of writing unless otherwise noted. Market Matters does not make any representation of warranty as to the accuracy of the figures or prices and disclaims any liability resulting from any inaccuracy.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The Market Matters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports. Market Matters may publish content sourced from external content providers.

If you rely on a Report, you do so at your own risk. Past performance is not an indication of future performance. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.