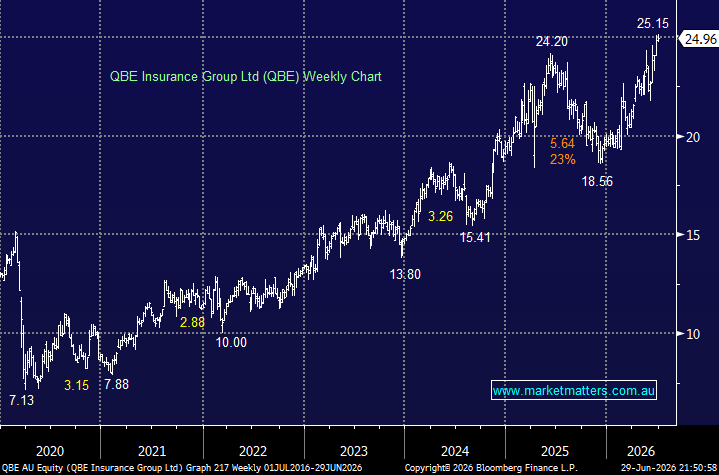

Insurer QBE has advanced +25% so far this year, hitting our initial ~$25 target area. Similar to WOW, we believe QBE is one of the ASX’s most compelling AI cost-saving opportunities. The February short & sharp sell-off on disruption fears missed the fact that insurance is ideally suited to AI, with claims processing, underwriting, fraud detection and customer service all ripe for automation. Given QBE’s global scale and complex legacy systems, even modest productivity gains should materially boost earnings, making AI more of a tailwind than a threat.

QBE is now trading at a premium to its long-term valuation, but its position to benefit from AI efficiencies, a solid US economy and a higher interest rate environment provide a healthy tailwind, as does its ~4.5% part-franked yield.

- We see no reason to take profit at this stage as the company evolves nicely from a recovery story into a consistent compounder. MM holds QBE in the Active Growth Portfolio.

MM is long and bullish towards QBE

Add To Hit List