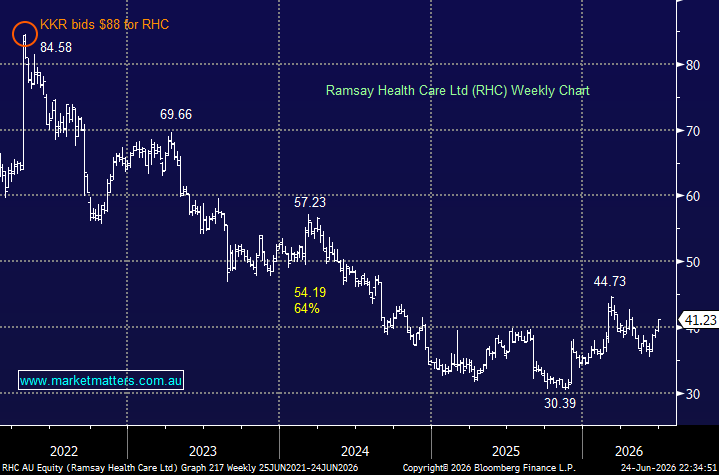

We covered RHC in detail back in Apil, here, and nothing has changed since with the stock trading 2-3% higher. Ramsay is a high quality business with attractive long-term fundamentals, but the operating environment remains challenging. The result has been lower returns and a more subdued earnings outlook than investors had become accustomed to before COVID, driving the significant derating in the stock, however on 25x, it’s not particularly cheap.

That said, with revenue set to improve by ~9% over the next 2 years, there is room for the company to improve earnings if/when it can better manage costs and thus improve margins. In simple terms, RHC could move the E in the PE equation more than markets think, and that would no doubt see the stock price continue to re-rate higher.

- We can see RHC testing the $50 resistance area in the coming year.

MM is cautiously bullish towards RHC around $41

Add To Hit List