Hi Bob,

Both PCI and DN1 are are designed to reduce equity market volatility, but they are not risk-free because they are exposed to credit and interest-rate risks.

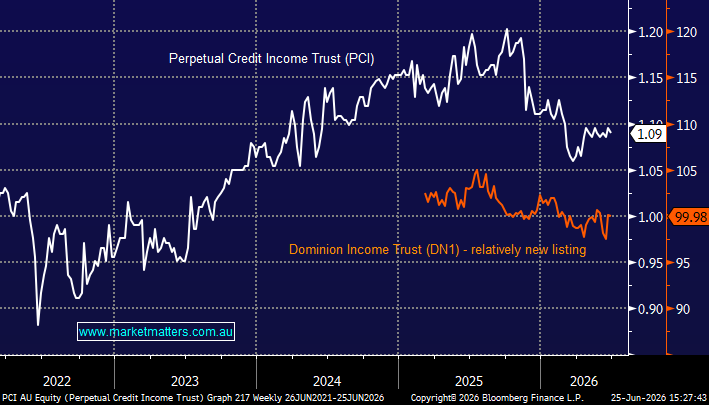

PCI, DN1, HBRD and YLDX all sit in the income part of a portfolio, but they don’t provide the same protection in a recession or bear market.

PCI and DN1 invest primarily in corporate credit and private debt. They generally exhibit much lower volatility than equities and continue paying income, but in a severe recession credit spreads usually widen, meaning their underlying assets can fall in value. They should decline much less than shares, but they’re unlikely to rise significantly as a hedge, and Govt bonds would perform better in this scenario.

HBRD invests in bank hybrids and now other subordinated debt due to the wind down of bank hybrids. These instruments sit between debt and equity in the capital structure. In a normal equity correction, they often hold up reasonably well, but in a banking or credit crisis hybrids can fall sharply because they’re designed to absorb losses before senior bondholders.

YLDX invests in floating-rate high-yield credit. Floating rates reduce interest-rate risk, but high-yield borrowers are more vulnerable in recessions, so credit spreads can widen materially and prices can fall.

If the goal is a true portfolio hedge against a deep recession or depression, high-quality government bond funds (Australian Commonwealth or US Treasury bonds) have historically provided the strongest protection because their prices often rise as investors seek safety and central banks cut interest rates.

Importantly, credit and debt funds are not hedges. They provide reliable income in normal and moderate-stress environments, but they correlate more with equities in a genuine sell-off relative to Govt bonds. If the goal is volatility hedging, the only instruments that genuinely deliver that in a recession are government bond duration, or cash, plus on occasion gold.