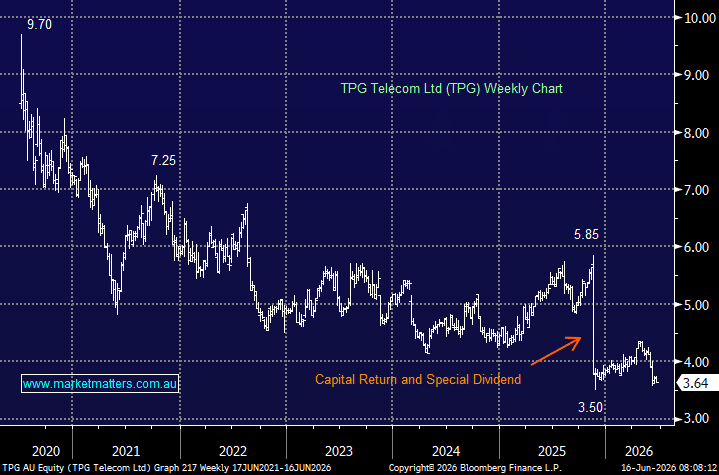

TPG has really disappointed since COVID, although things aren’t as bad as they look at a glance, following the sale of TPG’s fibre assets to Vocus for $5.25 billion, which led to one of the largest capital management initiatives seen on the ASX in recent years, with approximately $3 billion returned to shareholders through a capital return and special dividend, in the process shoring up the company’s balance sheet. TPG’s fibre sale looks even smarter today than it did when announced, with the company now a pure mobile play at precisely the moment when mobile is the most defensible part of the telco stack.

By comparison, and similarly, Telstra no longer owns the fixed-line infrastructure underpinning its broadband business, having sold those assets to NBN Co. That leaves both Telstra and TPG relatively insulated from any migration to satellite broadband, while the biggest long-term loser could prove to be NBN Co itself, which has spent more than $50 billion building a network that Starlink may increasingly challenge in regional Australia – the government’s massive NBN expenditure looks like a another big mistake – no wonder they now need to tax us more!

TPG’s decision to back Lynk and AST SpaceMobile rather than Starlink is an interesting strategic choice. It preserves commercial independence and avoids paying a potential competitor, but it also means the timing and scope of its satellite offering remain less certain than some rival solutions. For investors, the bigger issue is execution. Following the fibre asset sale, TPG has become increasingly reliant on mobile growth, leaving management with less room for error in an already competitive market.

- We cannot get excited around TPG despite its likely well-timed sale to Vocus.

MM is neutral towards TPG around $3.60

Add To Hit List