Hi Nick,

Thanks for the feedback, always much appreciated by the MM Team.

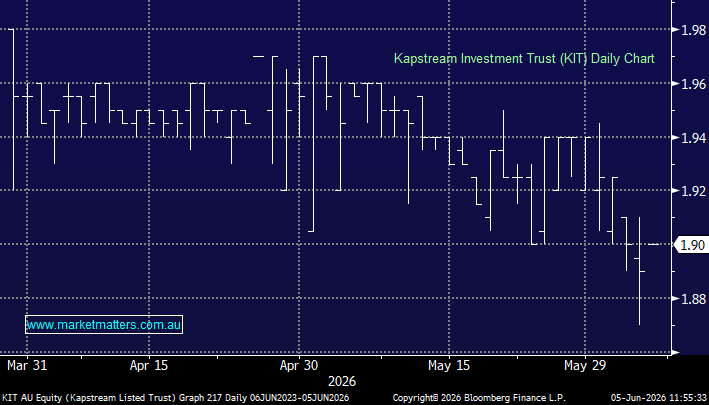

Firstly, with KIT we have to be careful reading too much into day to day moves because the liquidity is low for the freshly listed LIC. KIT’s buyback structure should be viewed as a feature of the vehicle, not a warning sign. KIT can offer an off-market buy-back where unitholders can elect to sell some or all of their units back to the trust, rather than selling on-market. The buy-back would be conducted quarterly, and at NTA.

In other words, the mechanism was built in from day one because the managers understood that LITs can trade below asset backing and wanted a tool to address it. With NTA at $2.0064 as at 25 May, a $1.90 share price implies a discount of around 5%, not huge, but we’ll see how the off-market buy back goes in June. They will cap it at ~5% of issued units we think.

As for bank hybrids, they are benefitting from a scarcity premium at the moment, and tight credit spreads. They are also a very different structure to a listed trust. We have seen plenty of times when Hybrids have traded below par in the past, however, given APRA’s rule changes, we know banks are going to redeem them on first call dates, and this makes them safer than the LIT’s – so they should therefore trade on a lower yield (higher price).