What would be highest conviction equity positioning

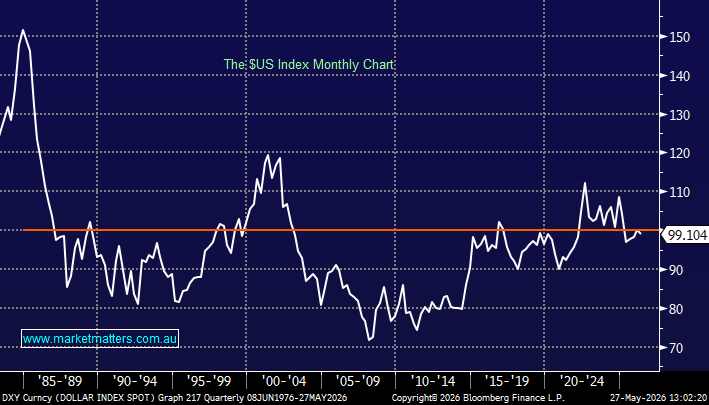

I follow your incisive newsletter every day and have found your analysis stimulating and informative. While you often focus on macro analysis, I feel it is very US focussed naturally, but the rising power of China is often missed. I have been following Andre Jikh’s incisive analysis of geopolitics and the global monetary system, he makes some fascinating points. Recently he posted a detailed analysis across macro economics and finance and doesn’t believe that “Trump went to China to deliberately crash the dollar”. He believes in a broader hypothesis: the meeting may have been part of a larger effort to rebalance the global monetary order in a way that reduces pressure from U.S. debt dynamics. Jikh frames it as a possible modern version of the 1985 Plaza Accord — sometimes discussed in macro circles as a “Mar-a-Lago Accord” concept — where the U.S. would seek a controlled weakening of the dollar rather than allow an uncontrolled adjustment later. Variants of this theory have been discussed by market commentators and policy observers, though many aspects remain speculative rather than established policy. His argument can be summarised in several linked ideas: • The U.S. debt problem is becoming structurally harder to finance. Large and growing debt levels require continual Treasury demand. If interest costs keep rising, debt servicing itself becomes a larger fiscal burden. • The reserve currency role creates both privilege and burden. The U.S. benefits because the world needs dollars and Treasuries, lowering borrowing costs and allowing persistent deficits. But global demand for dollars can also keep the dollar stronger than would otherwise occur, making exports less competitive and contributing to trade imbalances. • A moderately weaker dollar could relieve pressure. A weaker dollar can: make U.S. exports more competitive, reduce the real burden of nominal debt over time through inflation and currency depreciation, encourage domestic manufacturing and reshoring. But this only works if the decline is gradual and trusted. A disorderly loss of confidence could instead raise Treasury yields and worsen debt costs. The larger geopolitical implication is where the analysis becomes more interesting. Reserve currencies are not just economic tools; they are geopolitical infrastructure. Dollar dominance allows the U.S. to: Fund deficits more cheaply, impose sanctions with global reach, influence capital flows, shape trade settlement systems. Just look at what the demise of the pound as a reserve currency did to the British Empire in the 1950s. Countries such as China have spent years trying to reduce dependence on this architecture through gold accumulation, bilateral trade settlement in local currencies, and yuan internationalisation efforts. Yet replacing the dollar is much harder than many narratives imply because reserve currencies depend heavily on deep capital markets, legal institutions, liquidity and trust. Even critics of U.S. policy note that there is currently no full-scale substitute. The most useful takeaway from Jikh's analysis may not be Trump wants a weaker dollar. The more important question is whether the U.S. is attempting to preserve dollar dominance by reshaping the rules before markets force a reshaping anyway. Assume Andre Jikh's thesis is directionally correct: that U.S. policymakers are intentionally seeking a controlled depreciation of the USD to manage debt sustainability and rebalance trade. What leading indicators over the next 12–24 months would confirm or invalidate this thesis? Specifically, which signals would you track across Treasury yields, term premium, DXY, foreign Treasury ownership, gold reserves, capital flows, and sector performance, and what would be the highest-conviction equity positioning if this scenario unfolds?