Long-duration assets, typically growth stocks, are investments where a large share of their value is derived from cash flows expected well into the future. They traditionally struggle when bond yields rise, as the present value of those future cash flows declines. The flip side is that shorter-duration value stocks — companies making money today, trading on low P/Es and paying dividends now — should be better placed to outperform.

In a well-timed move for today’s report, the Dow gained +0.3% overnight, while the NASDAQ retreated -0.5%, a night where value outperformed growth. However, we must remain conscious of the AI factor, which continues to skew pockets of the growth sector at present.

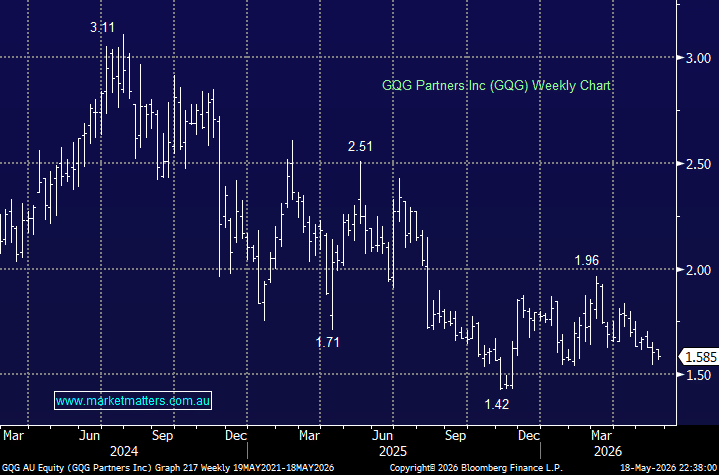

This morning, we’ve picked a quasi-way to play the “value over growth” outlook for the coming year, one where we believe plenty of risk is already baked into the cake. GQG has struggled since mid-2024 after transitioning its portfolios away from Big Tech too early in hindsight, but as long-term fund managers, their thesis remains in play. The subsequent underperformance relative to peers has led to some outflows, although, in our opinion, they have done a very good job articulating their non-consensus views and retaining investors.

We, and the market, do not expect GQG to show any real earnings growth over the next few years. The best-case scenario is that they maintain current earnings of around ~$430m annually. However, they are not priced for growth, and in an environment of higher inflation and higher rates, current earnings matter more.

GQG trades on ~8x earnings and yields north of 10% unfranked. The share price has come under renewed selling pressure as tech and AI have underpinned the recent rally in US stocks. Given GQG’s lack of meaningful exposure to this part of the market, it will likely report further short-term underperformance after a period of relative improvement in recent months. However, at the end of April, FUM sat at ~US$166.9bn and, as noted earlier, has remained very resilient despite material underperformance across the majority of its funds.

Right now, investors are scared not to own US tech, but this, like all markets, is cyclical. When investors go in search of value, GQG should re-rate quickly.

NB: The stock trades ex-dividend today.

- We believe GQG is a good example of a short duration value stock – MM owns GQG in its Active Growth Portfolio and in its Active Income Portfolio.

MM is long and bullish on GQG Partners around $1.60

Add To Hit List