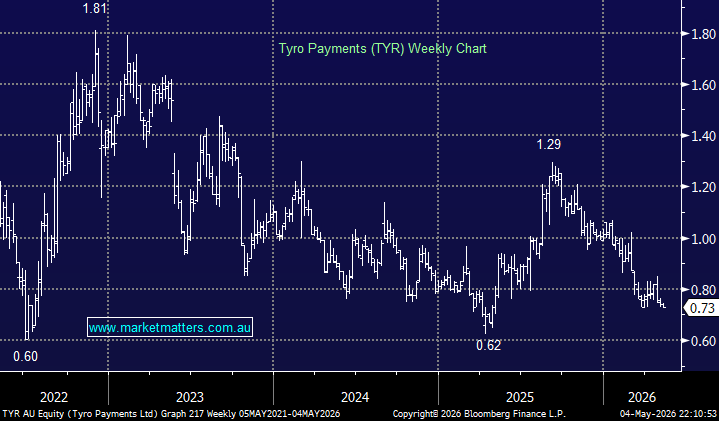

Fintech Tyro operates Australia’s largest non-bank network of payment terminals serving over 73,000 merchants in healthcare, hospitality and retail. It’s been growing revenue and gross profit steadily while keeping costs well-controlled. However, the stock has endured a tough few years, more than halving to become a relatively small $390mnn business.

- Tyro Payments makes money primarily by charging Australian small and medium-sized businesses a percentage fee, typically around 1.4%, on every card transaction processed through its EFTPOS terminals, with supplementary revenue from business lending and banking products.

The key issue for TYR has been regulatory, with the proposed ban on debit card surcharges weighing on the stock, a direct hit to Tyro’s revenue model, given that debit card transactions make up approximately 70% of card transactions in Australia. Ongoing uncertainty around the final rules has weighed on sentiment, although recent RBA reforms in March provided some clarity, with the stock rebounding slightly. Tyro also faces growing competition from large international players, including Block Inc. (NYSE: SQ), well-capitalised competitors with global scale and product breadth that Tyro cannot match.

- Tyro received a non-binding takeover approach from Private Equity firm Potentia and other co-investors in 2022 at $1.27, later raised to $1.60, the eventual rejection of the offers in May 2023 sent the share price sharply lower, a pattern almost identical to what happened with Bapcor Limited (ASX: BAP) and the Bain Capital approach.

The strategic logic is obvious: any global payments player (Worldline, Adyen, Stripe, or even a major Australian bank) wanting instant scale in Australian merchant acquiring would find Tyro’s 73,000-terminal network extraordinarily hard to replicate organically. Tyro is arguably cheap due to the regulatory uncertainty and already has a history of attracting acquisition interest. It’s important to remember that the business is actually profitable and growing revenue.

- We believe an offshore strategic buyer at a meaningful premium would be entirely logical.

MM is bullish towards TYR around 70c

Add To Hit List