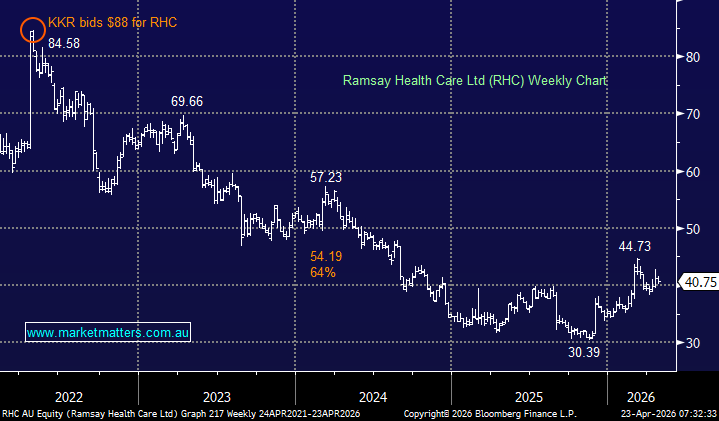

Ramsay Health Care (ASX:RHC) is one of the world’s largest private hospital operators, running hospitals, day surgeries and mental health facilities across Australia, Europe and the UK. Its business is straightforward: provide private healthcare services, from elective surgery and cardiac care through to rehabilitation and mental health treatment. In Australia, it’s a dominant force working closely with private health insurers; internationally, it expanded aggressively through acquisitions, particularly into Europe via its Ramsay Santé subsidiary, which created a tale of woe for the share price. The simple version — if you’ve ever had private surgery in Australia, there’s a good chance Ramsay owned the hospital.

Ramsay’s weakness has been driven by a combination of cost pressures, operational challenges, a disastrous expansion into Europe and a more difficult industry backdrop:

Cost inflation — margins squeezed: Hospitals are labour-intensive, and Ramsay has been hit hard by rising wages, nursing shortages and higher input costs. At the same time, revenue growth hasn’t kept pace, particularly in markets where pricing is regulated or negotiated, leading to sustained margin pressure.

Staffing shortages — capacity constraints: Like much of the healthcare sector, Ramsay has struggled with staff shortages post-COVID. This has limited its ability to fully utilise hospital capacity, reducing volumes and profitability.

Elective surgery disruptions (post-COVID hangover): COVID disrupted elective surgeries for years. While volumes have recovered, the rebound has been uneven, and backlogs have taken time to clear.

Weakness in key offshore markets: The UK (via Ramsay UK) has been a persistent drag, with operational challenges and weaker profitability. In Europe, while Ramsay Santé provides scale, it also exposes the group to more regulated healthcare systems with tighter margins.

Balance sheet & capital intensity: Hospitals are capital-heavy businesses. Ramsay carries significant debt following years of expansion, and higher interest rates have added pressure.

There is a two-fold lesson here, firstly, when ASX companies expand overseas, the risk/reward for investors diminishes dramatically and similarly, when stocks find themselves operating in a highly government-regulated environment, whatever the country. In both cases, adopting an if in doubt, sell would have added value to diversified ASX portfolios over the years.

Ramsay is a good business; demand for healthcare is structurally strong. However, it’s currently a tough operating environment for reasons touched on above. The result is a lower-return, more challenged earnings profile than investors were used to pre-COVID, and Ramay has rerated accordingly – it was only four years ago that KKR bid $88 for the stock, as is often the case, the board “cocked it up” by being too greedy, in hindsight, KKR were lucky. Ramsay has shifted from a steady compounder to a margin recovery story, and the market is waiting for further evidence that profitability can be sustained.

The company’s 1H result Here was very encouraging, and we believe the worst is behind RHC, but for investors second-guessing when to buy CSL and COH, note it took RHC four years to reach its nadir.

- We think the worst is behind RHC and the stock looks good into dips, but we wouldn’t yet be chasing strength.

MM is cautiously bullish towards RHC around $40

Add To Hit List