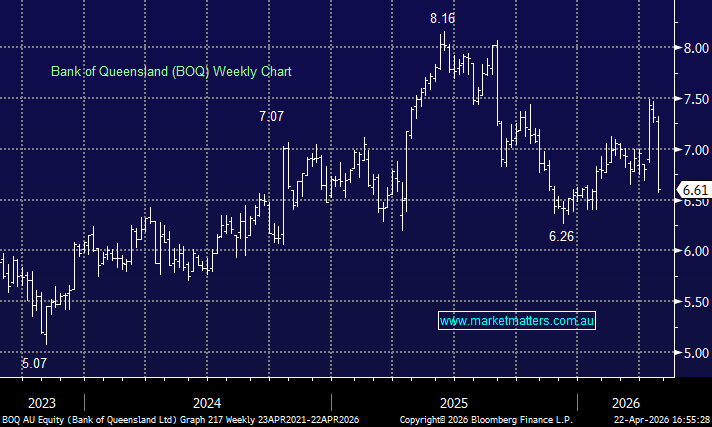

BOQ -9.1%: was hit today after delivering a softer-than-expected 1H26 result with cash earnings of $176m for the half, a slight miss to expectations, while the 20cps dividend was inline.

The result itself wasn’t a disaster, but it lacked the sort of clean improvement investors were hoping to see (and got with BEN recently) given the amount of change already underway across the group.

There are plenty of moving parts at the moment, and while new CEO Rod Finch only formally took the top job on 1 March 2026, he is hardly an outsider, having previously led transformation and operations.

- There were some better aspects to the update. Capital was stronger than expected, with CET1 at 11.2%, giving BOQ a useful buffer as it works through its broader simplification agenda.

We also saw continued momentum in digital channels, while improved disclosure around the equipment finance business was timely, particularly given the strategic Challenger partnership announced earlier this month. That transaction should help optimise funding, improve capital efficiency and support returns over time, though there can still be some statutory noise as it washes through the accounts.

UBS made the fair point that this result was struck before the recent escalation in Middle East tensions, meaning the operating backdrop may already have shifted by March. For a regional bank still trying to simplify, improve returns and win back market confidence, any increase in macro uncertainty is unhelpful. That leaves BOQ in an awkward spot: the balance sheet is holding up okay, but earnings momentum remains under pressure and sentiment is likely to stay fragile until management proves the transition is translating into more consistent delivery.

MM remains neutral on BOQ

Add To Hit List