Following RRL’s 1H earnings update the gold miner is expected to deliver strong shareholder returns, supported by $930m in cash and bullion plus robust free cash flow. The company plans to return 25–50% of its half-year cash increase as dividends, implying attractive yields of ~5.2% in FY26 and ~6.2% in FY27. Operationally, FY26 guidance of 350–380koz at AISC $2,610–2,990/oz remains unchanged, with the company on track after producing 187koz at $2,805/oz AISC in 1H. Importantly, no disappointing/mixed news as we heard from heavyweights NST and NEM.

Longer term, growth potential is centred on the McPhillamys project, which hosts a 2.26Moz resource and could generate an NPV of ~$1.15bn, with first production targeted around FY31, while additional upside may come from mine life extensions at Tropicana and Duketon.

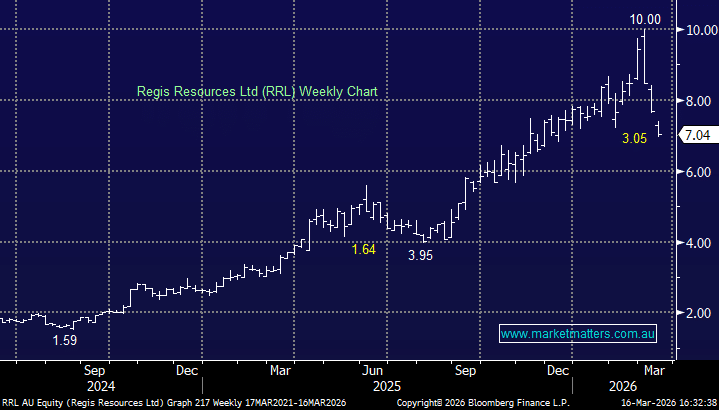

- We see good value in RRL after its ~30% pullback in recent weeks.

MM is bullish toward RRL around $7

Add To Hit List