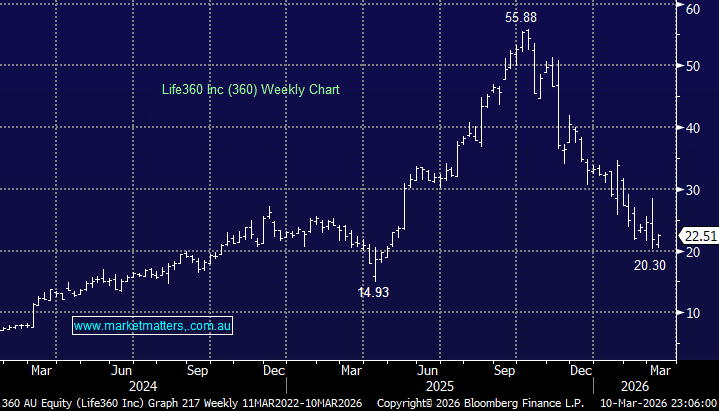

Life360 is doing what a growth stock should do – it’s growing. Revenue rose 32% in FY25 to $US489m, the company delivered its first full-year underlying profit, and management guided FY26 revenue to $US640–680m with monthly active users expected to hit ~115m. By any measure, that’s a compelling growth profile. Consensus was beaten. The business is scaling. The model is working. Yet the stock suffered a staggering 32% intraday reversal on result day, opening up ~15% before closing down ~17%. The re-rate has left the stock materially below where it should be trading, in MM’s view.

Two things spooked the market it seems. First, management flagged that user growth would be slower in the near term, with the bigger step-up expected in the second half. In high-growth names, even a temporary delay in momentum tends to get sold hard. Second, tariff uncertainty has thrown a wrench into Tile hardware manufacturing plans, with the shift out of China now on pause. Hardware is a shrinking part of the revenue mix (guided to just $40–50m in FY26), but uncertainty around margins and supply chains added to the nerves.

There’s also a broader AI overhang the market keeps returning to – the concern that AI-driven tools could replicate what Life360 does. Management pushed back firmly, and we think they have a point. Life360’s value is built on proprietary real-world data and embedded physical services like crash detection and roadside assistance. That’s not something a generic large language model displaces easily.

The fundamentals remain intact. Subscription revenue is growing solidly in both the US and internationally. Operating leverage is building. The mix is improving, shifting away from lower-margin hardware toward high-margin subscription and platform revenue. The business is now profitable. The re-rate looks like an overreaction in the short term, and at current levels, the risk/reward looks attractive. We are looking to add.

MM is looking to add to 360 ~$22

Add To Hit List