The flying kangaroo disappointed the market last week with its 1H numbers, with earnings from its international unit unexpectedly falling and the company flagging rising costs from wages and aircraft maintenance catching investors’ attention – covered Here. It would be an obvious call to have QAN in the avoid basket due to the conflict in the Middle East, but that’s just a compounding factor for MM, although “higher for longer” fuel prices will create a headwind for the airline.

The stock isn’t trading on a challenging valuation, plus it’s well supported by a ~6% yield, but we see the risks building and find the sidelines a more comfortable place to sit at this stage.

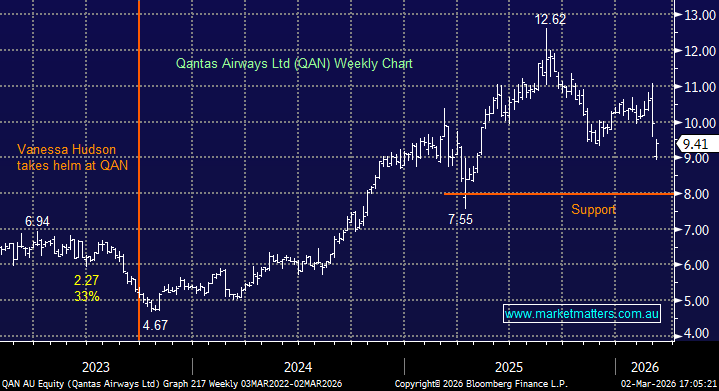

- We can see QAN testing back under $9, following its weaker 1H and the prospect of higher oil prices weighing on profitability.

MM is neutral at best towards QAN ~$9.40

Add To Hit List