This week the insurance industry witnessed a milestone with the launch of the first dedicated insurance app on ChatGPT, led by U.S. comparison platform Insurify, which enables users to research, compare and receive personalised car insurance quotes directly within the ChatGPT interface using conversational prompts. This follows approval of an AI insurance app by Spanish digital insurer Tuio that can generate real home-insurance quotes and, soon, even let users purchase a policy without leaving the ChatGPT chat window — a shift that could dramatically simplify the traditionally slow, form-heavy process of buying insurance and marks a new way insurers distribute products where consumers are already doing research.

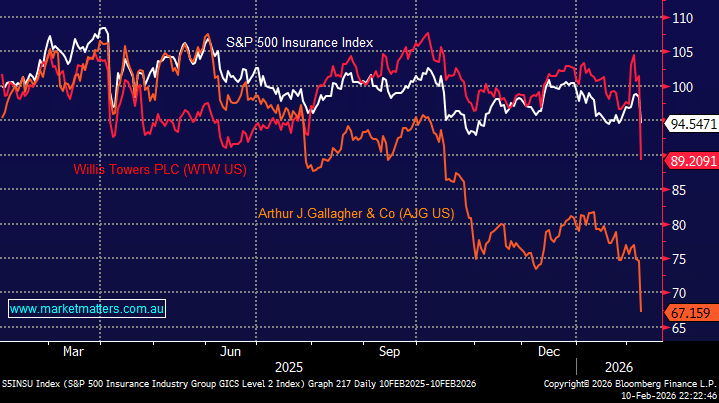

The result was instantaneous, with US insurance broker stocks smacked as the privately held online insurance shopping platform, Insurify, sparked fears about the industry facing disruption. The S&P 500 Insurance index closed down 3.9% on Monday, in its biggest drop since October. Insurance broker Willis Towers Watson PLC was the worst performer in the group, closing 12% lower and suffering its worst trading session since November 2008. Arthur J Gallagher & Co. followed with a 9.9% decline, and Aon PLC fell 9.3%.

- Our first take is that the middleman is in real danger from AI in many industries, including insurance, and we will be avoiding AUB Group (AUB) and Steadfast Group (SDF), having seen the damage done to software stocks by AI uncertainty.

These AI applications may be a threat to some insurance brokers/companies, but in some cases, they are expected to amplify and enhance existing capabilities, not replace or destroy them. Insurify’s app uses ChatGPT to compare auto insurance rates using details about the vehicle, the client’s credit history, driving record and other inputs. Again, we can see the middleman (brokers) being under pressure, but the interfaces at companies like QBE and NRMA should improve dramatically, potentially improving, not wrecking margins.

Looking at two of this week’s casualties, Willis Towers Watson (WTW US) and Arthur J. Gallagher (AJG US), they both generate revenue primarily by acting as intermediaries and advisers in the insurance ecosystem, but with slightly different mixes:

- Willis Towers Watson earns revenue mainly from insurance brokerage and consulting fees. Its largest business is commercial insurance brokerage, where it places insurance for corporate clients and earns commissions and fees from insurers and clients.

- Arthur J. Gallagher generates most of its revenue from insurance brokerage commissions and fees, particularly in property & casualty and employee benefits for mid-sized corporates, SMEs and niche industries.

As we alluded to earlier, we see the most potential disruption in the broker space with AI being able to replace years of experience and relationships, allowing end users, both large and small, to go straight to the source.

chart

US S&P 500 Index v Willis Towers (WTW US) & Arthur Gallagher (AJG US)

chart

US S&P 500 Index v Willis Towers (WTW US) & Arthur Gallagher (AJG US)

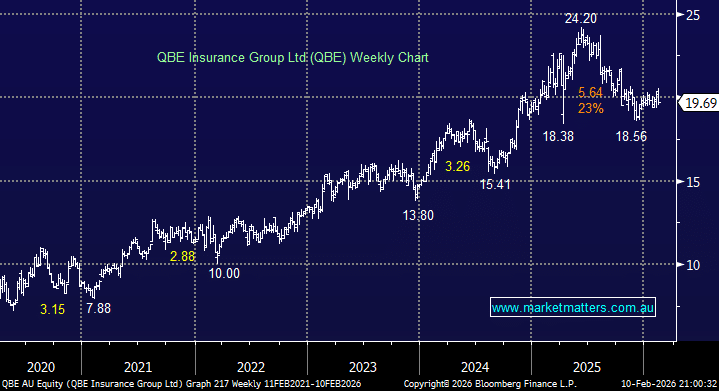

Shares in local insurance stocks also came under pressure on Tuesday with Sydney-based Steadfast (SDF) hit 9.5%, while rival insurance broker AUB (AUB) lost 6.1%, other major insurers were dragged lower in the slipstream from Suncorp (SUN) -4.2% to QBE -3.4%. Starting with IAG tomorrow, the local insurance sector faces the music this week although its unlikely to reveal whether they are at risk of disruption, they should speak more about the integration of AI into their business models.

- We believe the indiscriminate selling of the insurance sector will create an opportunity in the established insurers such as QBE, SUN and IAG.

However, we cannot ignore the risk from AI in any businesses with the following areas very real:

- Alternative data and AI-driven models could allow new entrants to selectively target the lowest-risk customers, potentially leaving incumbents like QBE with a poorer risk mix and heightened adverse selection unless they develop comparable capabilities. However, we could argue this happened to the banks with home loans from Aussie and Rams, and they’ve continued to flourish.

- More advanced analytics and AI underwriting could let competitors price risk more precisely and in real time, potentially eroding QBE’s advantage in commercial and specialty insurance.

- Both in claims and quoting, AI automation threatens to reset customer expectations on speed and experience, forcing QBE to invest to stay competitive.

Overall, AI is likely to intensify competition and erode returns for insurers slow to adapt, but for those that get it right, we can also see huge benefits. It’s not all bad news. For example, major insurers can strengthen their digital offering by rewarding loyalty with discounts for keeping multiple policies under one roof, appealing to consumers’ preference for clean, simple and consolidated experiences. Fortunately, QBE has become a far more efficient quality operator than a few years ago, when AI could have been a disaster for the “old QBE”.

- We bought QBE for our Active Growth Portfolio last week and continue to like the position and risk/reward towards the stock ~$20.

MM is long and bullish on QBE

Add To Hit List