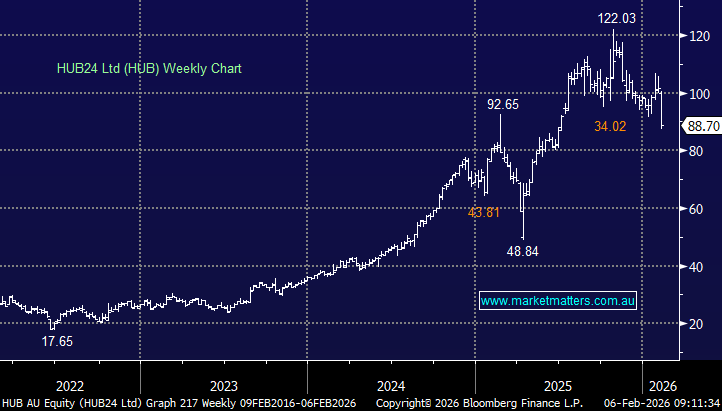

We are taking profit on HUB as we expect the valuation contraction to persist across tech. While we love the business, the stock is susceptible to a broader rerate that’s playing out across growth.

MM is selling HUB in the Active Growth Portfolio, taking profit around $88

Add To Hit List

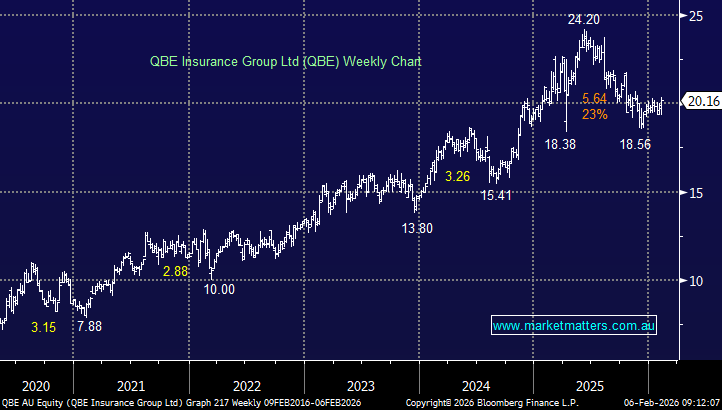

QBE is well positioned for reasonable growth, priced on a reasonable earnings multiple. Reducing tech, increasing insurance, is a clear move down the risk curve.

MM is buying QBE in the Active Growth Portfolio, allocating 4% around $20

Add To Hit List