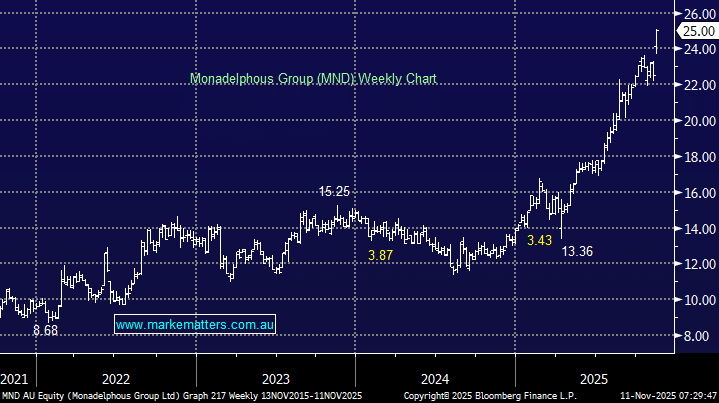

MND is an engineering company that’s best known for building and maintaining processing plants for major miners like BHP, Rio Tinto, and Fortescue, and for long-term shutdown and maintenance work that provides recurring revenue. On Monday, MND soared over +10% hitting levels not seen since 2013, after they flagged 1H revenue of ~$1.5bn, with FY revenue expected to be up +20-25% YoY. The stronger-than-expected revenue growth in FY26 is expected to be driven by heightened activity in its higher-margin engineering construction division. The contractor added that it’s getting a larger part of its revenue from vertically integrated construction projects, which leads to better margins and a stronger profit result. A quick upgrade followed by RBC lifting their PT 7% to $26.75.

With strong top-line growth leading to better margins and earnings, it’s easy to understand why MND has seen significant expansion in its earnings multiple – from ~19x up to ~25x. Such an expansion now leaves little room for error, making it hard to chase the stock at current levels, however, these are boom time businesses – they can make a lot of hay when the sun is shining, which is clearly the case now.

- We like MND but from a risk/reward perspective are reticent to chase it after a great run.

MM is cautiously bullish towards MND

Add To Hit List