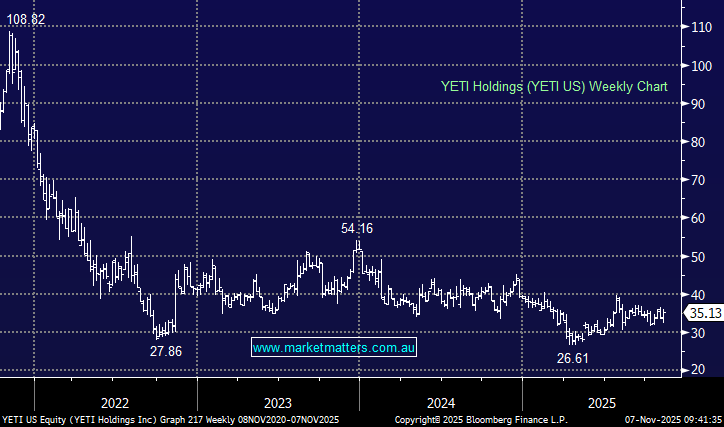

YETI delivered a solid 3Q25 result overnight, with earnings coming in mildly ahead of expectations, though, they were still down YoY.

- Sales grew 1.9% y/y to $487.8m, slightly ahead of consensus

- 3Q adjusted EPS of $0.61 beating expectations (vs $0.59 est)

Direct-to-consumer was the standout, up +2.8% y/y to $289m, a very positive signal for brand strength and margin preservation. Coolers & Equipment posted strong growth at +12% y/y to $215m, well ahead of estimates, but Drinkware sales fell 4.1% y/y, a drag that’s becoming more evident as the category matures. Management lifted FY share buyback target to $300m, and narrowed FY EPS guidance to $2.38–2.49 from $2.34–2.48, implying cautious optimism.

MM remains long and bullish YETI US

Add To Hit List