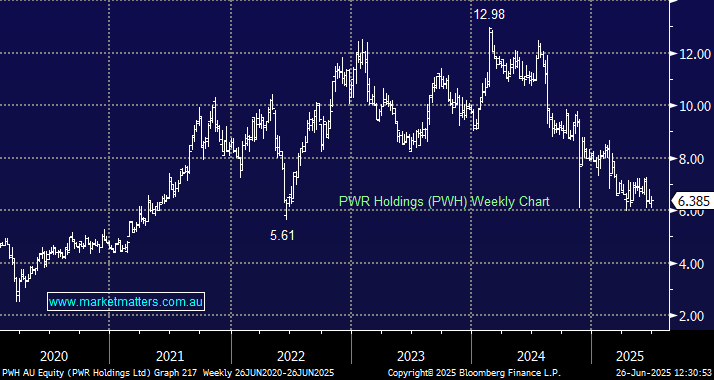

PWR Holdings (PWH)

PWH looks like a high quality business going through a rough patch. The share price has fallen significantly and the value proposition appears compelling. What do you think?

Our Q&As are emailed in our Saturday Morning Report, find the answer to this question below.

PWH looks like a high quality business going through a rough patch. The share price has fallen significantly and the value proposition appears compelling. What do you think?

Hi Cameron,

For subscribers not familiar with PWH, it’s a $640mn QLD company that specialises in the design, engineering, and manufacture of advanced cooling solutions used in Motorsport (formula 1 for example), auto, aero & defence. The companies shares have halved from their 2024 highs for two primary reasons:

PWH faces further short-term profitability challenges due to strategic investments but its pick up in aerospace & defence areas positions it for potential growth in FY26 and beyond – revenue is forecast to increase by over 22%v in next year. Having moved on from elevated EV expectations, like many companies, PWH is trading on an ok valuation ,with some upside already built into the share price.

Take a free trial.

No payment details required.

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

A link to create a new password will be sent to the email address you have registered to your account.

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.