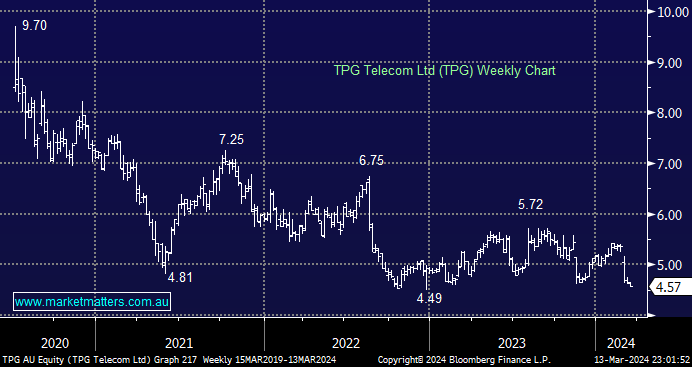

TPG delivered another poor result in February, with margins under pressure from increasing competition and debt/interest issues. Our stance hasn’t changed; we prefer TLS for income and ABB for growth, with TPG simply in the “too hard basket.”

- We see no reason to catch this falling knife until further notice.

MM has no interest in TPG

Add To Hit List