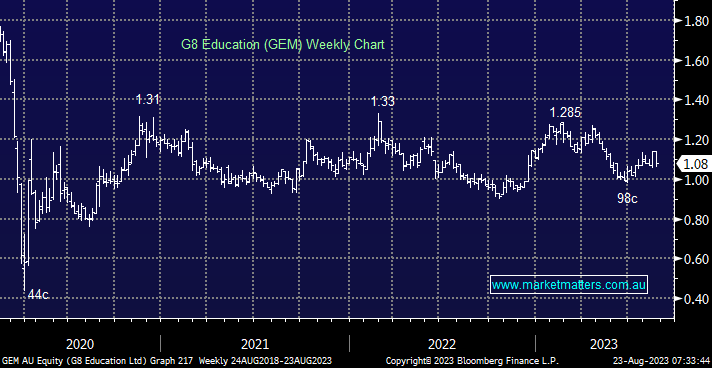

The childhood education and care provider with over 430 centres is one of the largest in Australia with a particular focus down the East Coast, although they also have some centres in WA. They operate under brands such as Jellybeans, Greenwood, Kool Kids, Bambinos and more, and while the last few years have been very challenging, to say the least, they are in a lot better position than they were 2 years ago and yesterday’s 1H23 result showed that. While occupancy remains too low (67.4%) and the improvement from the same time last year (+0.6%) is too benign, they continue to be constrained by ongoing labour shortages while the staff they have are being paid more through a recent award increase of 5.75%. New centre supply across the sector has also ticked up meaningfully, with the highest rate of new centre supply since 1H21, which adds competition for both staff and children. Adding further complexity, there are results due from an ACCC review targeting fee increases of providers across the industry which adds another layer of uncertainty to the already challenging backdrop, plus a declared dividend for the half of 1.5c fully franked was not enough of a reason to hold.

- While we think GEM is doing a good job turning around, a lot of external challenges remain that create a higher degree of uncertainty in the near term, prompting us to cut the position.

MM has sold GEM from the Income Portfolio

Add To Hit List