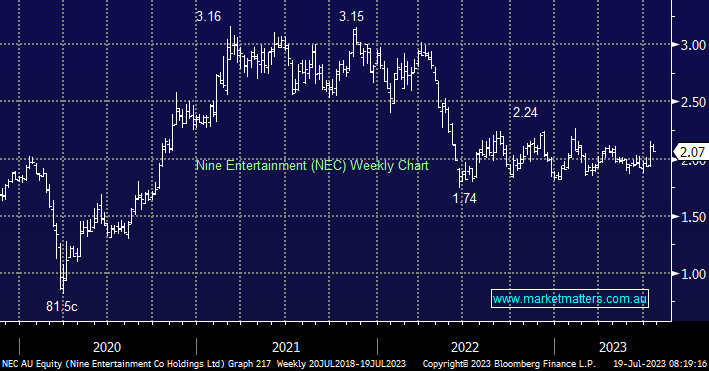

Monthly media data for June was released this week, showing a continuation of the decline in ad spending, largely across the board. TV ad bookings fell -15.7% yoy in the month which compares to Nine’s guidance for around a 15% decline at an update in May. Bookings for FY23 were down -12.4%, though it is important to note the numbers are cycling a very strong FY22, and a slowdown was expected. This clearly creates a headwind for earnings in the case of Nine Entertainment where around 60% of earnings (EBITDA comes from TV and Radio. Analysts have priced in a ~15% drop in EBITDA for FY23, and NEC trades on ~13x PE, meaning it is cheap and priced for the ongoing headwind in our view. However, it’s harder to see a catalyst to push the stock higher, more likely to come from growth in Stan or Domain Holdings (DHG) rather than the traditional media business lines Nine runs.

MM is neutral NEC, looking to take profit ideally around $2.20.

Add To Hit List