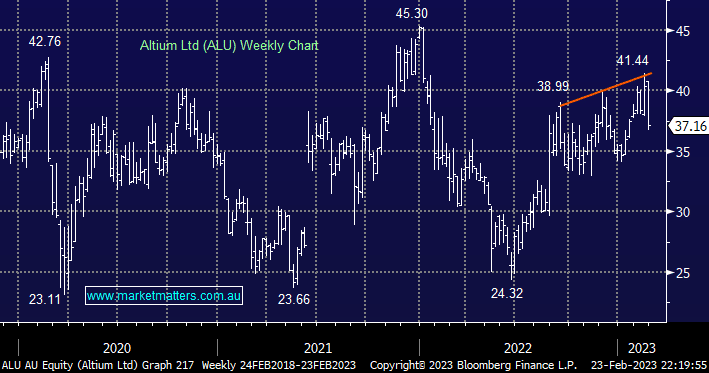

Earlier in the week printed circuit board design software provider delivered its 1H23 result which was a touch light for the pedantic investor but they maintained their FY23 guidance for revenue of $255-265m i.e. a growth rate of 15-20% on FY22. The stock has fallen in almost opposite fashion to WTC after positioning itself positively into the release.

- We believe ALU has suffered more because it rallied into its result as opposed to operating issues.

MM is still looking to trim/sell ALU at higher levels

Add To Hit List