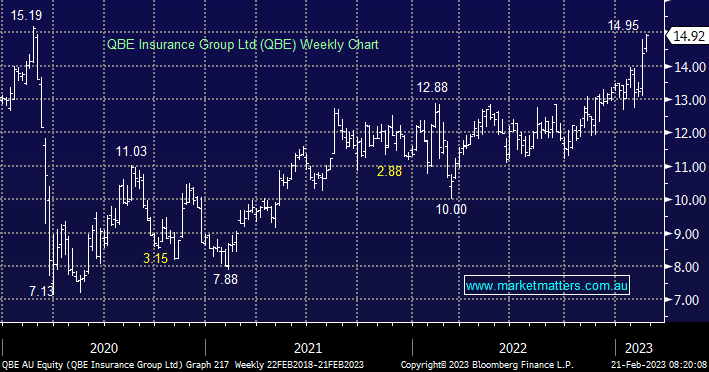

Our current pick across our banks & insurers is QBE, with their FY22 result demonstrating the turnaround that MM believes is unfolding across the business. In our opinion, the share price is still not reflecting the tailwinds they have from a macro perspective aided by a logical simplification of the company from an operational standpoint i.e. they are now focussing in areas where they ‘have an edge’. QBE is trading on around 11x, a discount to the banking sector when insurers generally trading at a premium.

- Whilst we would love to buy QBE into dips this is one stock that we may need to chase.

MM likes QBE below $15

Add To Hit List