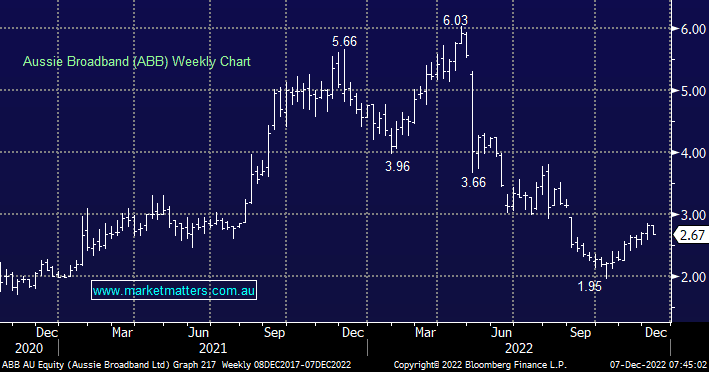

Our largest weighting in the Emerging Companies Portfolio has struggled over the past year, although since we flagged it as a conviction buy it is up ~15% to be the top performer on the list. Likely changes to wholesale NBN pricing are a positive and is the recent catalyst for the move higher, however, this is a company all about growth in connections at a high rate while maintaining margins. A very well-managed business that does sensible things with a medium to long-term focus i.e. it is not simply trying to appease the market in the short term. Good management with Phil Britt at the helm and looking to the outer years of estimates, this is a stock trading on ~14x with 20% earnings growth.

MM is bullish on ABB & would buy ~$2.70 if we did not already own

Add To Hit List