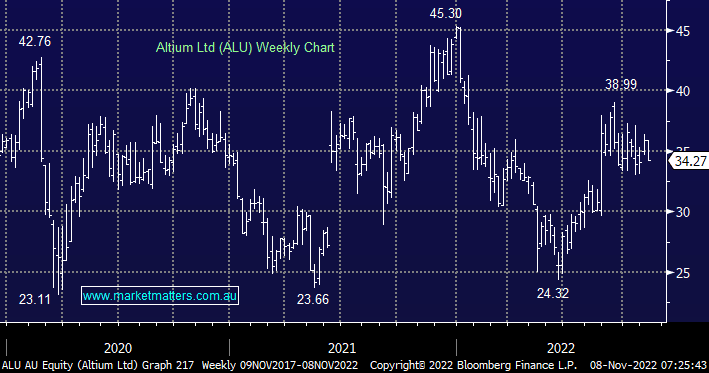

The Printed Circuit Board (PCB) design platform reported stellar FY22 results in August, revenue was $221m and EBITDA $81.1m while their FY23 guidance was also significantly better than consensus which dovetails nicely with our buy underlying operational strength and avoid those that disappoint mantra for 2022, especially in the growth names.

- We like ALU looking for around 20% upside but it’s likely to need some overall buying to wash through growth names to achieve our target.

MM is long and bullish ALU looking for levels above $40

Add To Hit List