Sell off continues ahead of a big week for markets

A busy weak ahead on a number of fronts with a truck load of quarterly production reports from the miners while we have also have some top tier economic data both here and abroad. In terms of production numbers, Iluka (ILU) and Newcrest (NCM) were out today, both were good while tomorrow we have Oz Minerals (OZL) and Western Areas (WSA), while fellow Nickel coy Independence Group (IGO) comes out on Wednesday along with St Barbara (SBM) then Fortescue (FMG) headlines on Thursday (along with Macquarie’s AGM).

On the economic front, PMI’s from the Eurozone and the US out tonight, inflation data from Australia on Wednesday along with a decision on US interest rates before we round out the week with US GDP on Friday. Clearly a big week for markets and we’ve started on the back foot with market sold off fairly aggressively today - more so in the morning than the afternoon.

As we discussed in the Weekend Report, we have unfortunately now turned more cautious the ASX 200, at least over the next few months after the market has failed to adhere to the usual July Strength. We are now looking for a pullback towards the 5500 major support area which should provide an excellent risk / reward buying opportunity.

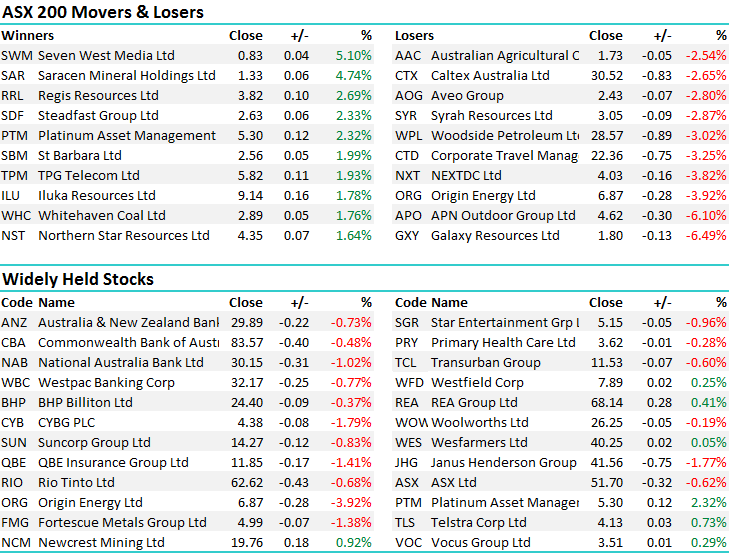

On the broader market today, the Telco’s were the only sector in the green which highlights what a weak mkt we had, while the Energy stocks gave back some recent gains, overall we had a range of +/- 70 points, a high of 5722, a low of 5653 and a close of 5688, off -34pts or -0.61%.

ASX 200 Intra-Day Chart

ASX 200 Daily Chart

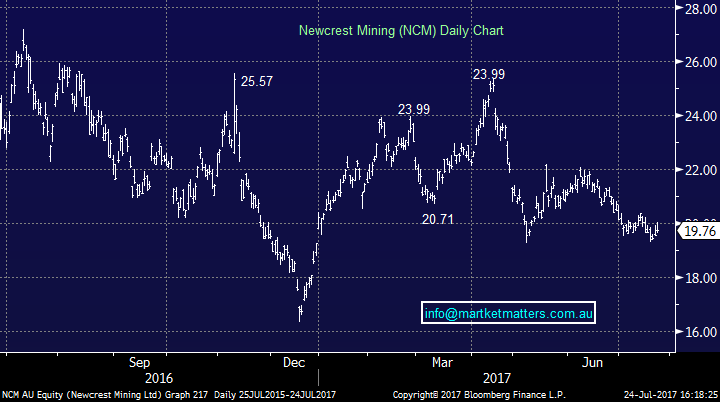

Newcrest (NCM) – delivered June QTR production numbers today and they were weakish in aggregate however came in ahead of mkt expectations. Weakness was anticipated given the disruption from their Cadia mine around Orange, however the actual impact was less than the mkt thought. Lihir hit a record and now looks to be humming along and importantly, NCM has now met/beat guidance for the past 4 years which is a massive turnaround from prior years. It helps to actually have mine managers on the ground in Lihir , even though it is very remote. Clearly a good turnaround from NCM in the last few years - the stock is cheap and Gold is offering some decent tailwinds.

Newcrest (NCM) Daily Chart

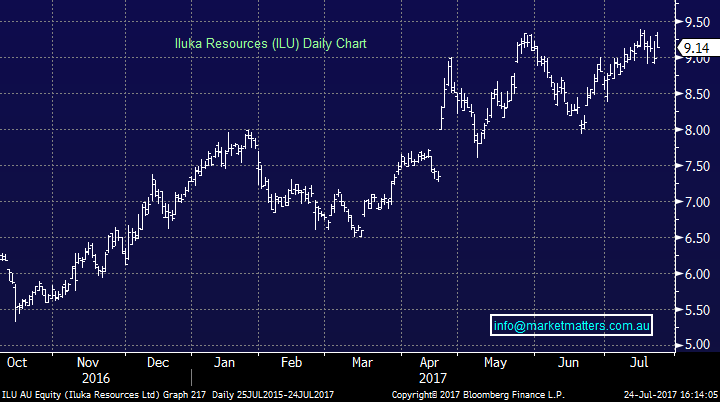

Iluka (ILU) - also out with qtrly production numbers that were slightly ahead of expectations, however it looked like the mkt was already positioned for a beat - ILU opened strong and pulled back for the session and this stock is now looking overcooked from a short term perspective. Recent commentary by other companies has been positive and Iluka was the same today, saying….Improved mineral sands market conditionswere evident in the first half of 2017 compared to 2016. Both the zircon and titanium feedstock markets experienced favourable conditions in 2017. Z/R/SR sales volumes up 43% to 454kt, excluding Sierra Rutile volumes, Z/R/SR sales volumes up 23%.

The debt reduction in this business has been huge in recent times, with $360m annualised in free cash flow and debt down by $200m since December. We like ILU however would look to buy weakness rather than strength.

Iluka (ILU) Daily Chart

Have a great night

The Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday.

Disclaimer

All figures contained from sources believed to be accurate. Market Matters does not make any representation of warranty as to the accuracy of the figures and disclaims any liability resulting from any inaccuracy. Prices as at 24/07/2017. 5.00PM.

Reports and other documents published on this website and email (‘Reports’) are authored by Market Matters and the reports represent the views of Market Matters. The MarketMatters Report is based on technical analysis of companies, commodities and the market in general. Technical analysis focuses on interpreting charts and other data to determine what the market sentiment about a particular financial product is, or will be. Unlike fundamental analysis, it does not involve a detailed review of the company’s financial position.

The Reports contain general, as opposed to personal, advice. That means they are prepared for multiple distributions without consideration of your investment objectives, financial situation and needs (‘Personal Circumstances’). Accordingly, any advice given is not a recommendation that a particular course of action is suitable for you and the advice is therefore not to be acted on as investment advice. You must assess whether or not any advice is appropriate for your Personal Circumstances before making any investment decisions. You can either make this assessment yourself, or if you require a personal recommendation, you can seek the assistance of a financial advisor. Market Matters or its author(s) accepts no responsibility for any losses or damages resulting from decisions made from or because of information within this publication. Investing and trading in financial products are always risky, so you should do your own research before buying or selling a financial product.

The Reports are published by Market Matters in good faith based on the facts known to it at the time of their preparation and do not purport to contain all relevant information with respect to the financial products to which they relate. Although the Reports are based on information obtained from sources believed to be reliable, Market Matters does not make any representation or warranty that they are accurate, complete or up to date and Market Matters accepts no obligation to correct or update the information or opinions in the Reports.

If you rely on a Report, you do so at your own risk. Any projections are estimates only and may not be realised in the future. Except to the extent that liability under any law cannot be excluded, Market Matters disclaims liability for all loss or damage arising as a result of any opinion, advice, recommendation, representation or information expressly or impliedly published in or in relation to this report notwithstanding any error or omission including negligence.

To unsubscribe. Click Here