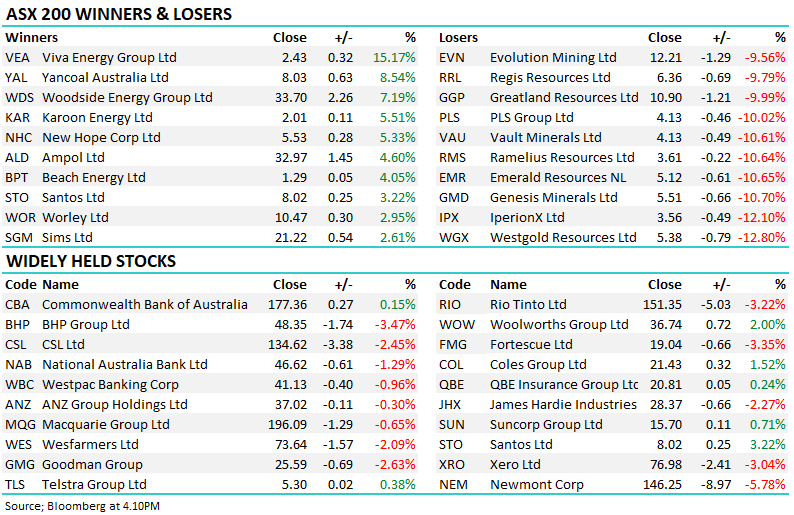

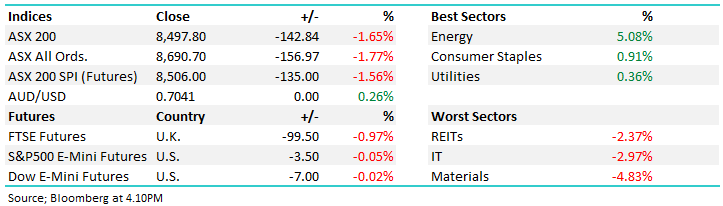

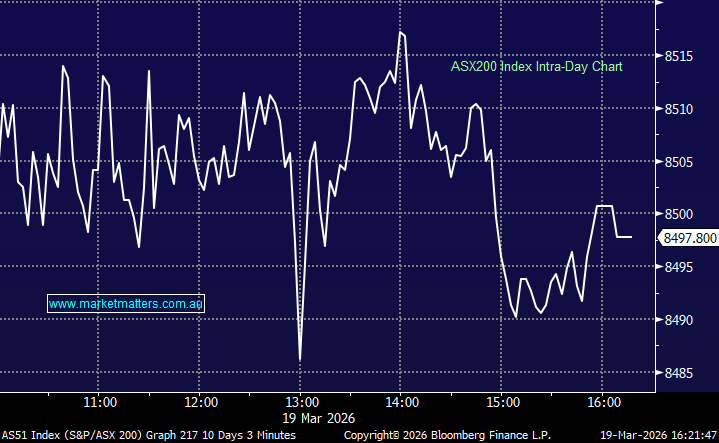

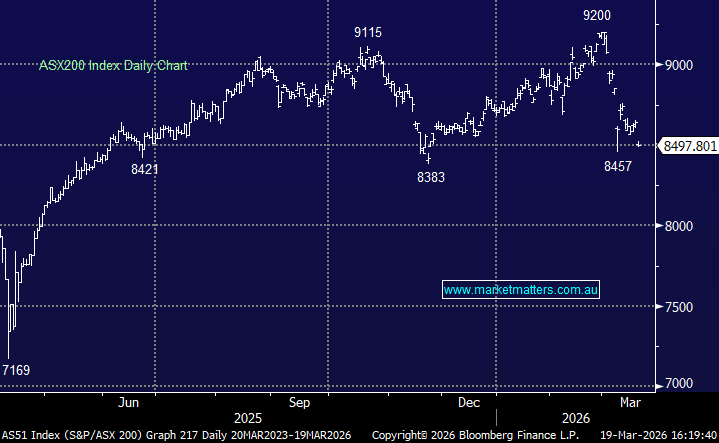

Last week saw the ASX200 post its worst week since September 2022, falling over 3%, as soft earnings in key areas, such as the influential banking sector, more than offset an improvement in the mining sector. Friday's 0.3% fall was the market's fifth consecutive losing day, its largest five-day point and percentage decline since early August.

Last week, the ASX200 climbed +0.5%, notching fresh highs on Thursday and Friday. However, on both occasions, the market surrendered most of the day's gains by the close. It was a mixed affair on the sector front, with the Industrials +2.9 % and consumer staples +2.4% leading the line while the healthcare -3.8% and energy stocks -1.1% took the open spoon. However, the real action unfolded on the stock level as is typical during reporting season:

The ASX200 slipped slightly in the first week of February ending down -0.24% with the healthcare and utilities sectors weighing on the market while the tech and materials stocks helped limit losses. It was an overall turbulent week for stocks as earnings season kicks into gear. The prospect of lower interest rates, trade war jitters and resilient consumer spending added to the day-to-day volatility. Local shares closed out the week flat with a negative tilt as traders remained cautious ahead of the US Payrolls report, which will influence the Fed's decision on interest rate cuts.

The ASX200 closed at its highest ever level, surpassing its previous record set 8 weeks ago. Friday saw the market gain another +0.45% extending January's advance to +4.57% with the rate-sensitive consumer discretionary, financials, real estate and tech sectors leading the charge. We are only five weeks into the new year, but the local market has already managed to dismiss the Trump inauguration and an AI shakeout courtesy of DeepSeek. Local stocks have followed European indices powering to fresh all-time highs, while US indices have struggled to advance year to-date under the weight of heavy AI selling, e.g. Heavyweight Nvidia (NVDA US) is down over 10% year-to-date.

The ASX200 ended a volatile and tough week, down 2.76% hitting a 100-day low on Friday. The Fed was the catalyst after cutting interest rates by 0.25% on Wednesday night, but at the same time, it moved the proverbial goalposts in terms of the future path in 2025. The Fed revised its outlook for rate cuts in 2025, indicating two reductions, down from the four previously forecasted in September.

The ASX200 ended the second week of December down by 1.48%, with the tech sector leading the retreat, tumbling by 5.7%. This was accompanied by real estate, financials, and industrials, which all declined by around 2%. The consumer staples and materials sectors were the only pockets to close up for the week, and they both advanced less than 0.1%. On the stock front, we saw some standout performance reversion from trends of 2024:

The ASX200 ended the first week of December down just 0.2%, with the real estate sector the main drag, falling 2.65% following the sell-down of $1.9bn worth of sector/market heavyweight Goodman Group (GMG) stock. Conversely, IT and consumer discretionary sectors were best on the ground. The gold names dominated the winner's enclosure after Northern Star's (NST) $5bn takeover of De Grey Mining (DEG), while lithium and ESG continued to decline.

The ASX200 ended the week up +0.5% and +3.38% for the month, and an even more impressive +3.9% when we include the chunky dividends in November. Through the penultimate month of the year, tech led the charge, advancing over 10%, while the materials and energy sectors were the only two to finish lower; it was a case of different month, but the same result for 2024.

The ASX200 ended the week over 1% higher after posting fresh all-time highs on Tuesday. The energy and Utilities sectors advanced over 4%, while the tech, real estate, and consumer discretionary sectors were the only three out of the 11 to lose ground. Under the hood, the gold and uranium miners stood out in the winner's enclosure while lithium stocks continued to decline - a theme that is not being mirrored in the United States with Albemarle (ALB US) up nearly 50% from its recent lows; elsewhere, cracks appeared in parts of the high-flying tech stocks. Company AGM’s as expected, threw up some volatility on the stock level:

Overseas indices ended the week poorly, with the post-election rally losing steam. The Dow ended over 300-points, while the NASDAQ led the decline, down 2.4%. European equities fared better, with the EURO STOXX 50 slipping 0.8 while the FTSE closed down just 0.1%. Declines in pharmaceutical stocks weighed on the Dow and the S&P 500, after Trump said he planned to nominate vaccine sceptic Robert F. Kennedy Jr. to lead the U.S. Department of Health and Human Services.

Last week, the ASX200 climbed +0.5%, notching fresh highs on Thursday and Friday. However, on both occasions, the market surrendered most of the day's gains by the close. It was a mixed affair on the sector front, with the Industrials +2.9 % and consumer staples +2.4% leading the line while the healthcare -3.8% and energy stocks -1.1% took the open spoon. However, the real action unfolded on the stock level as is typical during reporting season:

The ASX200 slipped slightly in the first week of February ending down -0.24% with the healthcare and utilities sectors weighing on the market while the tech and materials stocks helped limit losses. It was an overall turbulent week for stocks as earnings season kicks into gear. The prospect of lower interest rates, trade war jitters and resilient consumer spending added to the day-to-day volatility. Local shares closed out the week flat with a negative tilt as traders remained cautious ahead of the US Payrolls report, which will influence the Fed's decision on interest rate cuts.

The ASX200 closed at its highest ever level, surpassing its previous record set 8 weeks ago. Friday saw the market gain another +0.45% extending January's advance to +4.57% with the rate-sensitive consumer discretionary, financials, real estate and tech sectors leading the charge. We are only five weeks into the new year, but the local market has already managed to dismiss the Trump inauguration and an AI shakeout courtesy of DeepSeek. Local stocks have followed European indices powering to fresh all-time highs, while US indices have struggled to advance year to-date under the weight of heavy AI selling, e.g. Heavyweight Nvidia (NVDA US) is down over 10% year-to-date.

The ASX200 ended a volatile and tough week, down 2.76% hitting a 100-day low on Friday. The Fed was the catalyst after cutting interest rates by 0.25% on Wednesday night, but at the same time, it moved the proverbial goalposts in terms of the future path in 2025. The Fed revised its outlook for rate cuts in 2025, indicating two reductions, down from the four previously forecasted in September.

The ASX200 ended the second week of December down by 1.48%, with the tech sector leading the retreat, tumbling by 5.7%. This was accompanied by real estate, financials, and industrials, which all declined by around 2%. The consumer staples and materials sectors were the only pockets to close up for the week, and they both advanced less than 0.1%. On the stock front, we saw some standout performance reversion from trends of 2024:

The ASX200 ended the first week of December down just 0.2%, with the real estate sector the main drag, falling 2.65% following the sell-down of $1.9bn worth of sector/market heavyweight Goodman Group (GMG) stock. Conversely, IT and consumer discretionary sectors were best on the ground. The gold names dominated the winner's enclosure after Northern Star's (NST) $5bn takeover of De Grey Mining (DEG), while lithium and ESG continued to decline.

The ASX200 ended the week up +0.5% and +3.38% for the month, and an even more impressive +3.9% when we include the chunky dividends in November. Through the penultimate month of the year, tech led the charge, advancing over 10%, while the materials and energy sectors were the only two to finish lower; it was a case of different month, but the same result for 2024.

The ASX200 ended the week over 1% higher after posting fresh all-time highs on Tuesday. The energy and Utilities sectors advanced over 4%, while the tech, real estate, and consumer discretionary sectors were the only three out of the 11 to lose ground. Under the hood, the gold and uranium miners stood out in the winner's enclosure while lithium stocks continued to decline - a theme that is not being mirrored in the United States with Albemarle (ALB US) up nearly 50% from its recent lows; elsewhere, cracks appeared in parts of the high-flying tech stocks. Company AGM’s as expected, threw up some volatility on the stock level:

Overseas indices ended the week poorly, with the post-election rally losing steam. The Dow ended over 300-points, while the NASDAQ led the decline, down 2.4%. European equities fared better, with the EURO STOXX 50 slipping 0.8 while the FTSE closed down just 0.1%. Declines in pharmaceutical stocks weighed on the Dow and the S&P 500, after Trump said he planned to nominate vaccine sceptic Robert F. Kennedy Jr. to lead the U.S. Department of Health and Human Services.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.