The ASX 200 ended the week up +1.4 %, taking the month's gains to +2.7%, as the index pushed within striking distance of February's all-time high. The energy and tech sectors drove the gains, both ending the week by more than 5%, while defensive/rate-sensitive stocks dragged the chain, i.e. “risk on” was the order of the day. Out of the mainboard's 11 sectors, only the consumer staples, Utilities, and real estate sectors closed lower. The US-China “Trade Truce” set the platform for a strong start to the week, before the Australian market posted its highest level in three months on Friday after soft US economic data paved the way for interest rate cuts in Australia and the United States. The positive statistics are continuing to line up:

The ASX 200 ended a relatively quiet week down just 0.1%, not a bad effort considering ANZ and Westpac (WBC) delivered slightly softer 1H25 results, and WBC traded ex-dividend. Positive tariff news from the UK and US, plus optimism that something positive will come from the pending early talks between the US and China, supported a fairly lacklustre market, which remained in a tight 1.3% range all week. With news flow from Trump 2.0 relatively slow, the market was primarily keying off stock-specific news from reporting and the Macquarie Conference, leading to a very mixed bag in the “Winners & Losers” enclosure:

The ASX 200 surged another +3.4% last week, taking the main index up almost 15% from its April low, amazingly back within 4.4% of its February all-time high. We suspected “Offshore Buying” had been creeping into our market, and the last three sessions convinced us of it as the market again ended another week on its highs. All 11 main sectors finished the week higher, but a +9.6% surge by the tech sector stood out after strong earnings from US heavyweights Microsoft (MSFT US) and Meta Platforms (META US) re-ignited the “AI trade” and overall belief towards the tech/growth names:

Last week's wild gyrations on Wall Street shook investor confidence, but amazingly, US stocks wiped out early losses to deliver their best weekly gain since 2023. The Fear Index (VIX) spiked towards 60 on Monday before dropping to about 37 on Friday afternoon as relative calm returned to markets—a good sign into the weekend when posts can fly on X.

Financial markets went into “Panic Mode” on Friday night after China’s commerce ministry announced a 34% tariff on all U.S. products, disappointing investors who had hoped countries would negotiate with Trump. Xi Jinping has reacted “harder and faster” than markets expected, causing markets to plunge in a matter of seconds as fears of a Global Trade War escalated. Our take is Trump may be out of his depth; this is not a property deal. This feels like the US (Trump) versus the rest of the world! Selling intensified into the close on the fear, as we go into the weekend, that the trade war will escalate when the markets are closed, and the US doesn’t back down; it is very hard to see the US obtaining a good result from here, and Trump keeping face.

The ASX 200 enjoyed another positive week, although it will face a tough start on Monday following Friday's weakness in the US where the market was hit ~2%. On the sector front, there were some very different performances, with the finance sector gaining +2.6% while the tech names tumbled 3.3%.

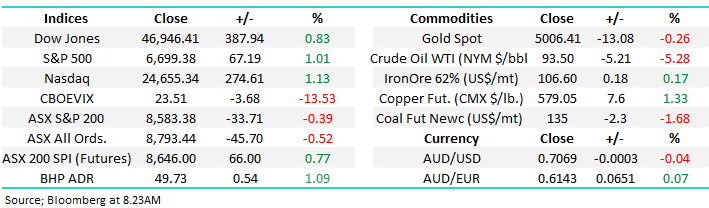

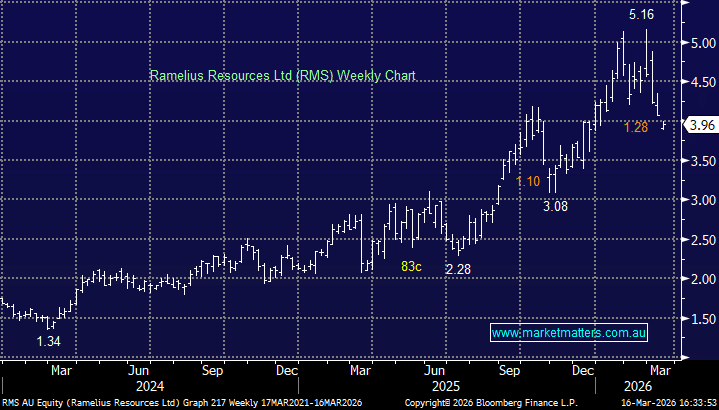

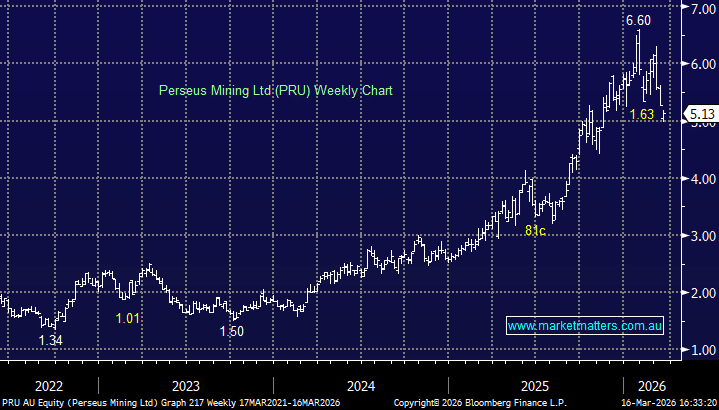

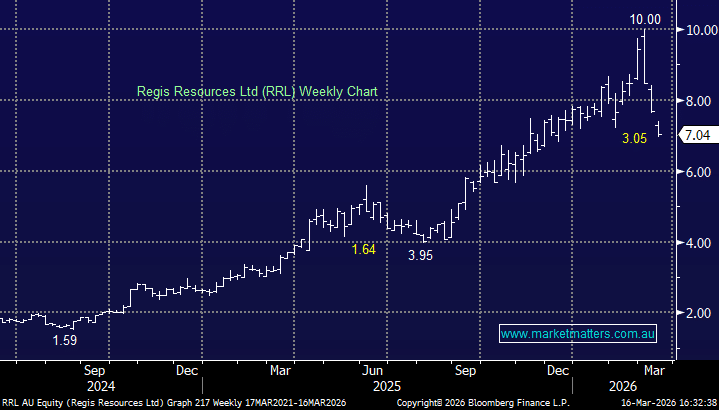

However, it was gold stocks that shone brightly as the precious metal surged another $US60, taking its gain in 2025 to over $US450, or 18%. Combined with a better week for the heavyweight iron ore miners, it was enough to help the Materials sector close higher again, albeit just. On the stock front, the winners and losers were very clearly defined:

It was a better week for local stocks, with the ASX 200 bouncing 1.8% on broad-based gains, which saw all 11 major sectors advance, led by an unusual combination of consumer staples and energy stocks. Following a tough four weeks, the Australian share market notched its best weekly positive performance of 2025, but with new tariffs due on April 2nd, it could still become the calm before the storm. The lack of fresh tariff news and encouraging developments on the interest rate front was enough to “stop the rot” in equity land, but how the market deals with the next wave of bad news will tell us the real story.

It was another tough week for local stocks, with the ASX200 closing down another 2%, extending the aggressive pullback to 10.2%, the market's largest 4-week decline since 2020. Eight of the eleven mainboard sectors declined, spearheaded by the tech, healthcare, consumer discretionary, and financial sectors, all of which fell over 3%. Performance reversion was again the main game in town, with the resources performing well at the expense of many high-flyers over the last year.

Friday's sharp 1.8% sell-off compounded what had already been a tough few weeks for local stocks. Last week saw the ASX200 accelerate lower, extending its decline from its mid-February high to 7.8%. Much of the damage was inflicted by the outperforming, high-value stocks that have driven markets over the last two years, such as banks, retailers and tech stocks.

Friday's sharp 1.2% sell-off compounded what had already been a tough February for local stocks. The ASX200 ended the month down 4.2%, with the Financials, Energy, Real Estate, Healthcare, and Tech sectors all falling over 5%. The defensives stood out in the winner's enclosure, with the Utilities +2.7% and Consumer Staples +1.5%, reducing the market's decline. The market's drop was its largest one-month decline since September 2022, as all the statistics aligned to paint a pretty average picture for investors, although we are still up for 2025, albeit just. On the stock level, the major movers were dictated by reporting season; next week should be back to normal, although we do still have Trump and an election looming:

The ASX 200 ended a relatively quiet week down just 0.1%, not a bad effort considering ANZ and Westpac (WBC) delivered slightly softer 1H25 results, and WBC traded ex-dividend. Positive tariff news from the UK and US, plus optimism that something positive will come from the pending early talks between the US and China, supported a fairly lacklustre market, which remained in a tight 1.3% range all week. With news flow from Trump 2.0 relatively slow, the market was primarily keying off stock-specific news from reporting and the Macquarie Conference, leading to a very mixed bag in the “Winners & Losers” enclosure:

The ASX 200 surged another +3.4% last week, taking the main index up almost 15% from its April low, amazingly back within 4.4% of its February all-time high. We suspected “Offshore Buying” had been creeping into our market, and the last three sessions convinced us of it as the market again ended another week on its highs. All 11 main sectors finished the week higher, but a +9.6% surge by the tech sector stood out after strong earnings from US heavyweights Microsoft (MSFT US) and Meta Platforms (META US) re-ignited the “AI trade” and overall belief towards the tech/growth names:

Last week's wild gyrations on Wall Street shook investor confidence, but amazingly, US stocks wiped out early losses to deliver their best weekly gain since 2023. The Fear Index (VIX) spiked towards 60 on Monday before dropping to about 37 on Friday afternoon as relative calm returned to markets—a good sign into the weekend when posts can fly on X.

Financial markets went into “Panic Mode” on Friday night after China’s commerce ministry announced a 34% tariff on all U.S. products, disappointing investors who had hoped countries would negotiate with Trump. Xi Jinping has reacted “harder and faster” than markets expected, causing markets to plunge in a matter of seconds as fears of a Global Trade War escalated. Our take is Trump may be out of his depth; this is not a property deal. This feels like the US (Trump) versus the rest of the world! Selling intensified into the close on the fear, as we go into the weekend, that the trade war will escalate when the markets are closed, and the US doesn’t back down; it is very hard to see the US obtaining a good result from here, and Trump keeping face.

The ASX 200 enjoyed another positive week, although it will face a tough start on Monday following Friday's weakness in the US where the market was hit ~2%. On the sector front, there were some very different performances, with the finance sector gaining +2.6% while the tech names tumbled 3.3%.

However, it was gold stocks that shone brightly as the precious metal surged another $US60, taking its gain in 2025 to over $US450, or 18%. Combined with a better week for the heavyweight iron ore miners, it was enough to help the Materials sector close higher again, albeit just. On the stock front, the winners and losers were very clearly defined:

It was a better week for local stocks, with the ASX 200 bouncing 1.8% on broad-based gains, which saw all 11 major sectors advance, led by an unusual combination of consumer staples and energy stocks. Following a tough four weeks, the Australian share market notched its best weekly positive performance of 2025, but with new tariffs due on April 2nd, it could still become the calm before the storm. The lack of fresh tariff news and encouraging developments on the interest rate front was enough to “stop the rot” in equity land, but how the market deals with the next wave of bad news will tell us the real story.

It was another tough week for local stocks, with the ASX200 closing down another 2%, extending the aggressive pullback to 10.2%, the market's largest 4-week decline since 2020. Eight of the eleven mainboard sectors declined, spearheaded by the tech, healthcare, consumer discretionary, and financial sectors, all of which fell over 3%. Performance reversion was again the main game in town, with the resources performing well at the expense of many high-flyers over the last year.

Friday's sharp 1.8% sell-off compounded what had already been a tough few weeks for local stocks. Last week saw the ASX200 accelerate lower, extending its decline from its mid-February high to 7.8%. Much of the damage was inflicted by the outperforming, high-value stocks that have driven markets over the last two years, such as banks, retailers and tech stocks.

Friday's sharp 1.2% sell-off compounded what had already been a tough February for local stocks. The ASX200 ended the month down 4.2%, with the Financials, Energy, Real Estate, Healthcare, and Tech sectors all falling over 5%. The defensives stood out in the winner's enclosure, with the Utilities +2.7% and Consumer Staples +1.5%, reducing the market's decline. The market's drop was its largest one-month decline since September 2022, as all the statistics aligned to paint a pretty average picture for investors, although we are still up for 2025, albeit just. On the stock level, the major movers were dictated by reporting season; next week should be back to normal, although we do still have Trump and an election looming:

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.