A mixed bag across the board today with sectors split pretty much down the middle, however, the heavy-weight sectors dragged the overall index lower. Quarterly reports from the miners dominated the news flow though it was the softness in commodity prices that mostly weighed on the sector. BOQ copped a few downgrades overnight and concerns around bad debts and competition for mortgages put pressure on the financials sector. The ASX 200 was down -31pts/-0.42% for the week.

Another tepid session for stocks with the ASX down early before a spirited fightback saw the market trade up for the day, before some selling took hold into the close. At this stage, the market simply feels tired after its stellar run as opposed to being bearish and swamped with high-volume selling. Today the winners actually outnumbered the losers (just), although a ~2% decline by the material sector is always going to weigh, offset by a good move higher by the banks.

Another fairly flat session by the ASX today, although it’s looking tired and we wouldn’t be surprised to see a near-term top evolve with the first signs of money transitioning from the edgier, high-beta areas into the more defensive plays. Still, with negative market positioning (high cash levels + high bond ownership v equities) very obvious we wouldn’t be running for the hills, meaningful tops don’t often correlate with pessimistic positioning – but a pause, consolidation, and a shallow pullback could easily play out.

A slow day for the market with a lot of fundies away for School holidays + finding compelling value is getting harder given the market’s recent run. Sometimes it’s best to sit tight and it certainly felt that way today in what proved to be a choppy but overall negative session for stocks with 65% of the index closing lower.

The local market kicked off the new week by adding to recent gains, hitting a 2-month high in the process. Financials continued their recent form to boost the index, rallying on the back of a better-than-expected start to the quarterly updates from their US peers.

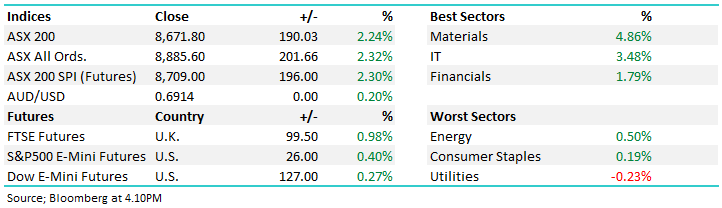

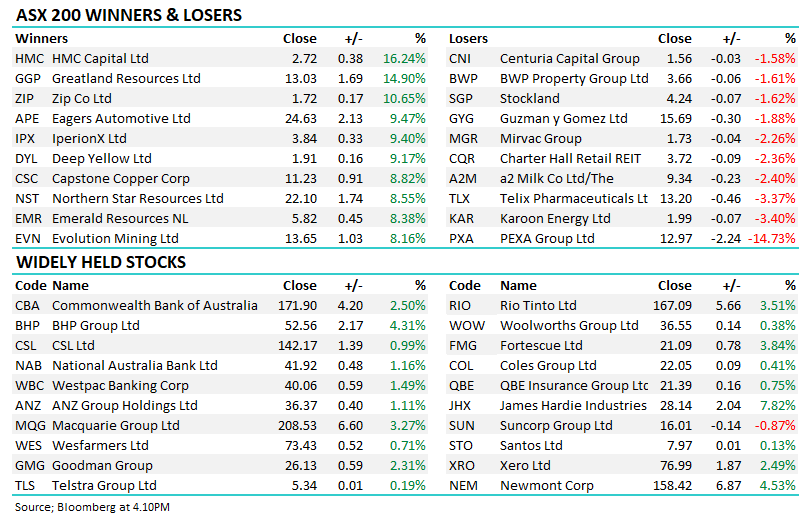

There was a delayed reaction to strength seen overnight on the local market today which rallied strongly out of early session lows. Materials were the standout with a broad rally from the sector, though Gold stocks were the key contributors as the precious metal cracked 1-year highs. Financials were also strong despite a soft update from one of the regional banks. Overall the ASX had a great week with all 11 sectors finishing higher, the index put on +142pts/+1.98% and is sitting around 5-week highs.

The market finally cooled today with a stronger-than-expected March employment report the catalyst which increases the chances of the RBA going one more time, although our expectation is they’ll sit tight at 3.60% come the May meeting.

Another solid session for the market today with Tech & Resources doing the heavy lifting, the ASX200 is now up ~450pts/6.5% from the 20th March low hitting a 5-week high, however, we get a major test tonight with US CPI Inflation data to be released, consensus expectations are for 5.1% YoY which would be the 9th consecutive monthly decline from a 9.1% peak in June 2021.

A few scratching their head on the desk around what’s driving the advance, perhaps traders took risk-off ahead of the 4-day break and the rare occurrence of important U.S. economic data being released on a public holiday, or perhaps corporate activity (Newcrest getting bid again) was the catalyst, whatever the case our view has been a more bullish one suggesting that surprises are more likely on the upside – today’s result certainly fit that view nicely!

The local market tracked lower as the day rolled on as investors took some risk off the table ahead of the long weekend. Most sectors were lower, but tech felt the brunt of the pain, Resources sectors were also soft and while Financials were down, they outperformed the weaker market. Healthcare and Utilities were the main standouts. The market gave up 45pts from its highs to briefly tip below 7200 again, before recovering around half of the fall in the last 2 hours of trade. As the Aussie market enters a 4-day weekend, US Employment data will be released tomorrow night and their equity market is open on Monday.

Another tepid session for stocks with the ASX down early before a spirited fightback saw the market trade up for the day, before some selling took hold into the close. At this stage, the market simply feels tired after its stellar run as opposed to being bearish and swamped with high-volume selling. Today the winners actually outnumbered the losers (just), although a ~2% decline by the material sector is always going to weigh, offset by a good move higher by the banks.

Another fairly flat session by the ASX today, although it’s looking tired and we wouldn’t be surprised to see a near-term top evolve with the first signs of money transitioning from the edgier, high-beta areas into the more defensive plays. Still, with negative market positioning (high cash levels + high bond ownership v equities) very obvious we wouldn’t be running for the hills, meaningful tops don’t often correlate with pessimistic positioning – but a pause, consolidation, and a shallow pullback could easily play out.

A slow day for the market with a lot of fundies away for School holidays + finding compelling value is getting harder given the market’s recent run. Sometimes it’s best to sit tight and it certainly felt that way today in what proved to be a choppy but overall negative session for stocks with 65% of the index closing lower.

The local market kicked off the new week by adding to recent gains, hitting a 2-month high in the process. Financials continued their recent form to boost the index, rallying on the back of a better-than-expected start to the quarterly updates from their US peers.

There was a delayed reaction to strength seen overnight on the local market today which rallied strongly out of early session lows. Materials were the standout with a broad rally from the sector, though Gold stocks were the key contributors as the precious metal cracked 1-year highs. Financials were also strong despite a soft update from one of the regional banks. Overall the ASX had a great week with all 11 sectors finishing higher, the index put on +142pts/+1.98% and is sitting around 5-week highs.

The market finally cooled today with a stronger-than-expected March employment report the catalyst which increases the chances of the RBA going one more time, although our expectation is they’ll sit tight at 3.60% come the May meeting.

Another solid session for the market today with Tech & Resources doing the heavy lifting, the ASX200 is now up ~450pts/6.5% from the 20th March low hitting a 5-week high, however, we get a major test tonight with US CPI Inflation data to be released, consensus expectations are for 5.1% YoY which would be the 9th consecutive monthly decline from a 9.1% peak in June 2021.

A few scratching their head on the desk around what’s driving the advance, perhaps traders took risk-off ahead of the 4-day break and the rare occurrence of important U.S. economic data being released on a public holiday, or perhaps corporate activity (Newcrest getting bid again) was the catalyst, whatever the case our view has been a more bullish one suggesting that surprises are more likely on the upside – today’s result certainly fit that view nicely!

The local market tracked lower as the day rolled on as investors took some risk off the table ahead of the long weekend. Most sectors were lower, but tech felt the brunt of the pain, Resources sectors were also soft and while Financials were down, they outperformed the weaker market. Healthcare and Utilities were the main standouts. The market gave up 45pts from its highs to briefly tip below 7200 again, before recovering around half of the fall in the last 2 hours of trade. As the Aussie market enters a 4-day weekend, US Employment data will be released tomorrow night and their equity market is open on Monday.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.