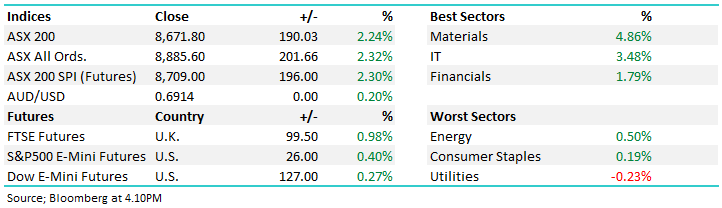

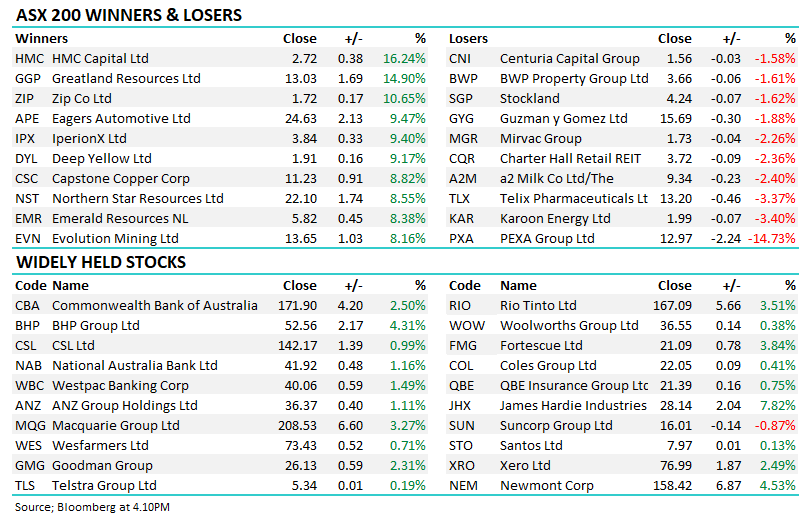

The vibe so far in reporting is a net positive one with more beats than misses, and more companies rallying post results despite some festering concern around what’s to come in FY24. That’s not to say everything is positive, but by-in-large, we’re doing okay and this was supportive of the ASX today which snapped a 2-day losing streak. Weaker data out of China continues to put pressure on the PBOC to stimulate, and while it remains largely elusive, the local resource stocks seemed to find some support from intra-day lows on optimism around such a move.

The ASX was hit today, weighed by growing concerns around the Chinese property sector as another large developer teeters on default - while earnings continue to dominate news flow locally. As of Friday, around 20% of the market’s total capitalisation had reported results, so far, so good with earnings beats outnumbering earnings misses by a solid ratio of 3:1, although we have seen adjustments lower for FY24 on softer outlooks.

A tentative end to a week that had a bit of everything, from company results here and overseas, important economic data, RBA testimony to parliament, a loss by Manly at Brookvale to end their season & now the biggest event of the week, the Matilda’s playing France on Saturday afternoon!

A solid day for the ASX as reporting threw up some more interesting candidates from a broad cross-section of industries, some hits, misses and a few in between, while we saw some action amongst the energy stocks with Crude breaking higher and Coal prices finding some support.

Shares started slowly today but found their mojo into the afternoon, finishing near highs on the back of strength in the banks. There was little change ahead of inflation data coming out of China mid-morning, but when that passed without concern, the focus returned to CBA’s record result.

The day started well with some reasonable buying across most major sectors however by midday, things had taken a turn and optimism was thin on the ground. A mixed bag from companies that reported results ahead of Commonwealth Bank (CBA) out with numbers tomorrow morning – we’ll cover them as they land.

A subdued start to the week with the ASX edging lower, void of any real impetus in either direction. A bank holiday, no influential companies reporting and a softer night on Friday in the States saw local investors sit largely idle, with winners and losers split evenly across the main board.

A quieter end to a more volatile week for equities with a US rating downgrade, continued volatility in bond markets, while overlapping quarterly earnings in the US and the start of FY reporting locally kept things interesting. Ultimately, stocks ended lower, bond yields were generally higher while commodities by in large remained resilient.

The ASX was down in line with overseas markets, although the selling was far from aggressive and we did bounce off the session lows. US Futures were subdued while Asian stocks were more mixed after a poor session yesterday.

A sea of red today from Shanghai to Sydney with stocks pulling back from recent highs, the RBA’s dovish move yesterday a distant memory as local reporting stumbles into gear.

The ASX was hit today, weighed by growing concerns around the Chinese property sector as another large developer teeters on default - while earnings continue to dominate news flow locally. As of Friday, around 20% of the market’s total capitalisation had reported results, so far, so good with earnings beats outnumbering earnings misses by a solid ratio of 3:1, although we have seen adjustments lower for FY24 on softer outlooks.

A tentative end to a week that had a bit of everything, from company results here and overseas, important economic data, RBA testimony to parliament, a loss by Manly at Brookvale to end their season & now the biggest event of the week, the Matilda’s playing France on Saturday afternoon!

A solid day for the ASX as reporting threw up some more interesting candidates from a broad cross-section of industries, some hits, misses and a few in between, while we saw some action amongst the energy stocks with Crude breaking higher and Coal prices finding some support.

Shares started slowly today but found their mojo into the afternoon, finishing near highs on the back of strength in the banks. There was little change ahead of inflation data coming out of China mid-morning, but when that passed without concern, the focus returned to CBA’s record result.

The day started well with some reasonable buying across most major sectors however by midday, things had taken a turn and optimism was thin on the ground. A mixed bag from companies that reported results ahead of Commonwealth Bank (CBA) out with numbers tomorrow morning – we’ll cover them as they land.

A subdued start to the week with the ASX edging lower, void of any real impetus in either direction. A bank holiday, no influential companies reporting and a softer night on Friday in the States saw local investors sit largely idle, with winners and losers split evenly across the main board.

A quieter end to a more volatile week for equities with a US rating downgrade, continued volatility in bond markets, while overlapping quarterly earnings in the US and the start of FY reporting locally kept things interesting. Ultimately, stocks ended lower, bond yields were generally higher while commodities by in large remained resilient.

The ASX was down in line with overseas markets, although the selling was far from aggressive and we did bounce off the session lows. US Futures were subdued while Asian stocks were more mixed after a poor session yesterday.

A sea of red today from Shanghai to Sydney with stocks pulling back from recent highs, the RBA’s dovish move yesterday a distant memory as local reporting stumbles into gear.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.