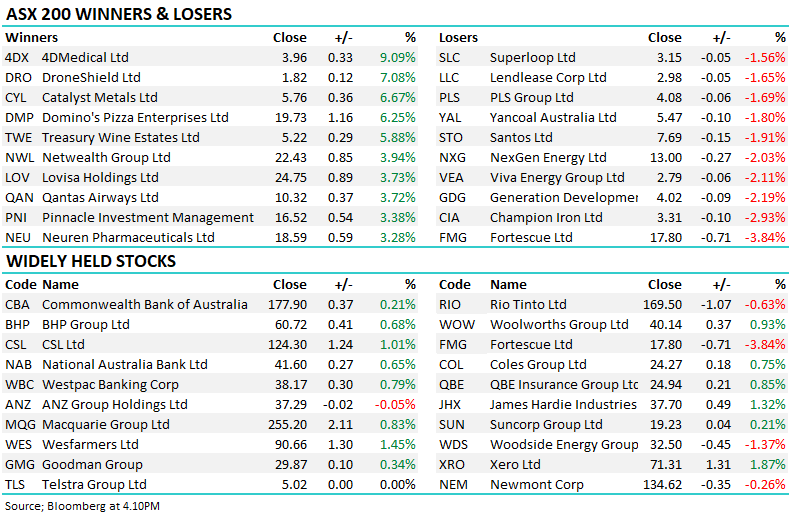

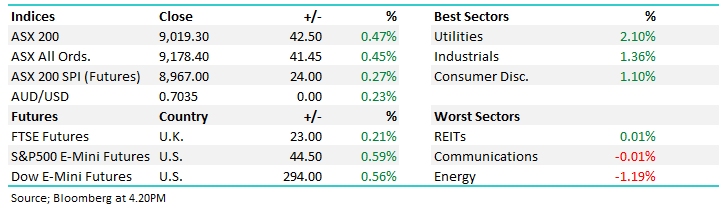

The ASX 200 recovered from a weak start to finish +42pts higher today, a good ~80pt turnaround from the lows with utilities, industrials and consumer discretionary stocks leading the advance. Australian futures had initially pointed to a decline of around 1%, but sentiment improved after President Donald Trump called off planned strikes against Iran and pushed for renewed negotiations, reducing the immediate risk of a larger regional conflict.

The ASX 200 finished modestly higher today, securing a fourth consecutive monthly gain despite giving back most of an early rally. The index traded as high as 9,059 before closing just +9 pts higher (down ~85pts from the open), with strong gains across materials, selected technology names and gold miners offset by weakness in healthcare, consumer staples and communications.

The ASX 200 snapped a three-day winning streak today, retreating from yesterday’s five-month high as investors reduced risk following a sharp sell-off in the US. Materials and consumer stocks under most pressure, although strength across technology and selected energy names helped cushion the decline.

The ASX 200 hit a five-month high today after softer-than-expected inflation all but removed the prospect of an August interest-rate hike with healthcare, consumer discretionary and consumer staples leading a broad-based rally.

A solid session locally, with the ASX 200 gaining 0.52% despite US futures remaining slightly lower. The move had the hallmarks of futures-led buying in Australia, with the SPI strengthening through the afternoon and broad gains across consumer discretionary, communications and healthcare, while the major banks also provided support.

The ASX kicked off the new week in fine form that to a pause in US-Iran strikes, putting some probability back on diplomacy. The early spike higher as US Futures rallied was held and built on as the day progressed. Oil traded down 6%, bond yields fell ~10bps and the US was sold, pushing the AUD back up through US70c.

The ASX 200 finished firmly lower today as renewed escalation in the Middle East pushed oil back toward US$100/barrel, reigniting inflation and interest-rate concerns. The Aussie 3-year bond yield was up +10bps to 4.72%, while the 10 year yield pushed through 5%, settling at 5.08%.

The ASX 200 finished a touch higher, though there was a big intra-day reversal following stronger employment data out at 11.30am. The index was up more than 100pts before giving back most of the rally as investors increased the odds of another RBA rate hike.

Australia added 76,000 jobs in June, well ahead of the 15,000 expected, while unemployment held at 4.4%. The result pushed the Australian dollar above US70¢ and the 10-year bond yield toward 5%, with markets now pricing a 36% chance of an August rate rise with a full hike priced in by year-end. Next week’s quarterly inflation data has now become even more important.

A reasonable day for the ASX as investors returned to beaten-down miners, with strength across copper, gold and energy stocks more than offsetting weakness in healthcare and technology. The buying was patchy though, with only 3 of 11 sectors trading higher, implying there is still a fair degree of caution out there.

Another session where the ASX was hit early before buyers stepped in, with the index recovering around 60 points from its two-week low to finish marginally higher. Technology and gold stocks led the rebound as investors bought the dip following recent weakness, while softer oil prices helped ease some concerns around inflation and the outlook for US interest rates.

Brent crude eased below US$89/barrel after rising almost 6% over the previous two sessions, while gold recovered toward US$4,050/oz. The improvement in offshore technology sentiment also helped, with US futures turning higher and Asian chip stocks rebounding after the sharp sell-off triggered by concerns around Moonshot’s Kimi K3 model.

The ASX 200 finished modestly higher today, securing a fourth consecutive monthly gain despite giving back most of an early rally. The index traded as high as 9,059 before closing just +9 pts higher (down ~85pts from the open), with strong gains across materials, selected technology names and gold miners offset by weakness in healthcare, consumer staples and communications.

The ASX 200 snapped a three-day winning streak today, retreating from yesterday’s five-month high as investors reduced risk following a sharp sell-off in the US. Materials and consumer stocks under most pressure, although strength across technology and selected energy names helped cushion the decline.

The ASX 200 hit a five-month high today after softer-than-expected inflation all but removed the prospect of an August interest-rate hike with healthcare, consumer discretionary and consumer staples leading a broad-based rally.

A solid session locally, with the ASX 200 gaining 0.52% despite US futures remaining slightly lower. The move had the hallmarks of futures-led buying in Australia, with the SPI strengthening through the afternoon and broad gains across consumer discretionary, communications and healthcare, while the major banks also provided support.

The ASX kicked off the new week in fine form that to a pause in US-Iran strikes, putting some probability back on diplomacy. The early spike higher as US Futures rallied was held and built on as the day progressed. Oil traded down 6%, bond yields fell ~10bps and the US was sold, pushing the AUD back up through US70c.

The ASX 200 finished firmly lower today as renewed escalation in the Middle East pushed oil back toward US$100/barrel, reigniting inflation and interest-rate concerns. The Aussie 3-year bond yield was up +10bps to 4.72%, while the 10 year yield pushed through 5%, settling at 5.08%.

The ASX 200 finished a touch higher, though there was a big intra-day reversal following stronger employment data out at 11.30am. The index was up more than 100pts before giving back most of the rally as investors increased the odds of another RBA rate hike.

Australia added 76,000 jobs in June, well ahead of the 15,000 expected, while unemployment held at 4.4%. The result pushed the Australian dollar above US70¢ and the 10-year bond yield toward 5%, with markets now pricing a 36% chance of an August rate rise with a full hike priced in by year-end. Next week’s quarterly inflation data has now become even more important.

A reasonable day for the ASX as investors returned to beaten-down miners, with strength across copper, gold and energy stocks more than offsetting weakness in healthcare and technology. The buying was patchy though, with only 3 of 11 sectors trading higher, implying there is still a fair degree of caution out there.

Another session where the ASX was hit early before buyers stepped in, with the index recovering around 60 points from its two-week low to finish marginally higher. Technology and gold stocks led the rebound as investors bought the dip following recent weakness, while softer oil prices helped ease some concerns around inflation and the outlook for US interest rates.

Brent crude eased below US$89/barrel after rising almost 6% over the previous two sessions, while gold recovered toward US$4,050/oz. The improvement in offshore technology sentiment also helped, with US futures turning higher and Asian chip stocks rebounding after the sharp sell-off triggered by concerns around Moonshot’s Kimi K3 model.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.