Hi Andrew,

Intuit is the dominant player in the US, its market cap of $US175bn v Xero’s $21bn puts things into perspective. Intuit generated more than $US17bn in US revenue in FY25 whereas Xero’s total international revenue was ~$US530mn. The play here is XRO taking market share is some specific areas that it is particuarly good at whereas Intuit’s size and complexity actually become weaknesses;

- Xero is simpler, cleaner, and more consistent across product tiers. It’s easier for Accountants to standardise workflows and imporve scale benefits in the SME space.

- QuickBooks (QB) – owned by Intuit, was built with inventory-heavy U.S. businesses in mind. Xero works better for consultants, creatives, tradies, contractors etc.

- XRO is a better integrator of third party applications, broadening it’s appeal, and is a lot more nimble than intuit, with fewer legacy issues.

Xero doesn’t need 50% market share in the U.S. to be successful; 5–10% U.S. penetration = a multi-billion opportunity achieved by focussing on verticals where QB isn’t optimal (e.g., creatives, consultants, digital agencies, franchise networks).

Matching Intuit’s scale is not the play here, it wins by being simpler, faster to adopt, and better for developers & accountants – plugging specific Intuit pain points – which are obvious around price, complexity, product sprawl, slow iteration etc. We think Xero can capture a profitable U.S. slice (5–10%) over 3–5 years.

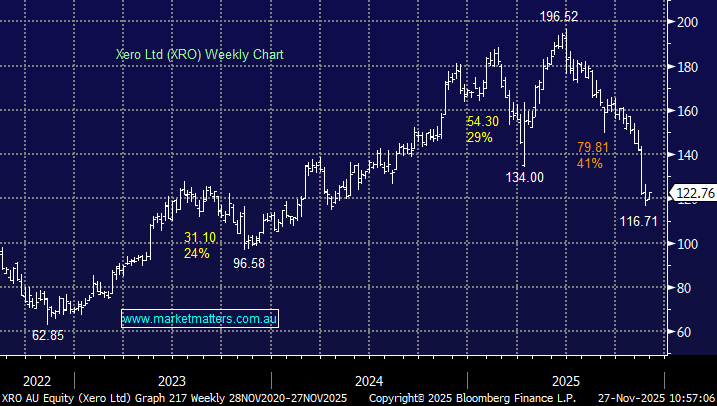

- We still like XRO at current levels.