Would MM consider adding PEN to its Emerging Company Portfolio?

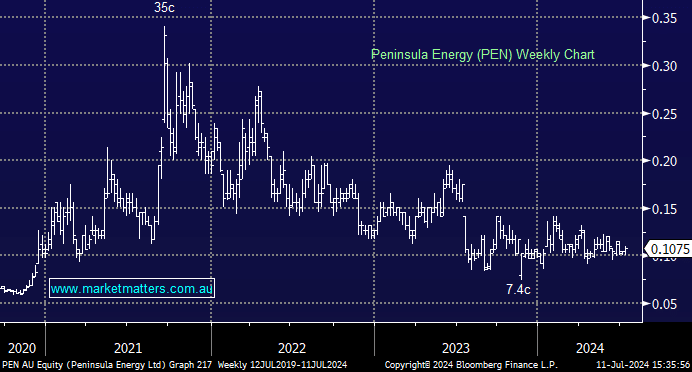

Hi MM, Is it correct that MM views PEN's funding risk as now being removed or largely removed (with development and construction risks remaining)? Assuming this to be the case, does MM view PEN as particularly cheap? Despite the improvement in PEN's cash position following the recent capital raise, it is still close to the capital raise price of $0.10 and does not seem to react to positive uranium developments/sentiment even when other uranium stocks rally in relation to such developments. I find this a little perplexing - does MM have a view on why this is the case; perhaps the capital raise still washing through, so to speak? Would MM consider adding PEN to its Emerging Company Portfolio? Thanks, Darren