Thoughts on HUB24 Ltd (HUB) and NRW Holdings (NWH)

Hi MM team, Please can you share your current thoughts on HUB and NWH? Thanks, JanP

Our Q&As are emailed in our Saturday Morning Report, find the answer to this question below.

Hi MM team, Please can you share your current thoughts on HUB and NWH? Thanks, JanP

Hi Jan,

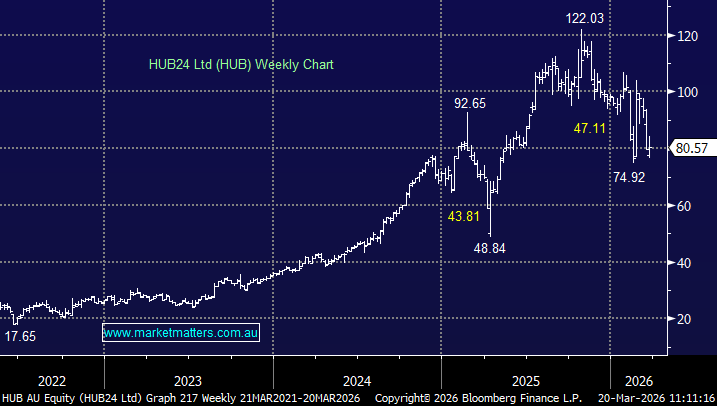

HUB24 (HUB) is a wealth platform provider that offers technology and administration services to financial advisers, enabling them to manage client investments and portfolios efficiently.

HUB24 is set to retain its #1 platform ranking (including Managed Accounts), driving above-peer growth in advisers, accounts and market share gains, outperforming Netwealth (NWL). Flows are increasingly coming from existing advisers as consolidation continues, reinforcing HUB’s scale advantages and operating leverage potential.

We continue to prefer HUB over NWL given stronger share gains, which partly justifies its valuation premium, though questions remain around long-term multiples amid AI disruption. We hear there are now several companies trying to build out investment platforms to compete with the incumbents – a tough ask in our opinion, but competition in the space will likely intensify, hopefully, driving better (& cheaper) alternatives!

NRW Holdings (NWH) is a mining services and civil contractor that provides contract mining, infrastructure and maintenance services to the resources and commercial sectors, earning revenue from project work rather than commodity prices.

NRW delivered a strong 1H26 result, with EBIT up +36% to $132m (~10% beat), driven by standout performance in the higher-margin METS segment, where revenue and margins exceeded expectations. Cash generation was solid, and momentum remains strong with a robust order book and pipeline i.e. the business has very strong momentum, which aligns with what we hear from our contacts operating in the space.

The company upgraded FY26 EBIT guidance to $275–285m, marking its third upgrade, highlighting continued strength in resources and infrastructure capex markets.

Take a free trial.

No payment details required.

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

A link to create a new password will be sent to the email address you have registered to your account.

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.